When US President Donald Trump imposed his so-called ‘retaliatory’ tariffs on 2 April, they had been widely anticipated. However, few were prepared for the scale of the tariffs and the way they were calculated. Even as financial markets reacted in panic, some of the immediate response was different from that during similar shocks this century.

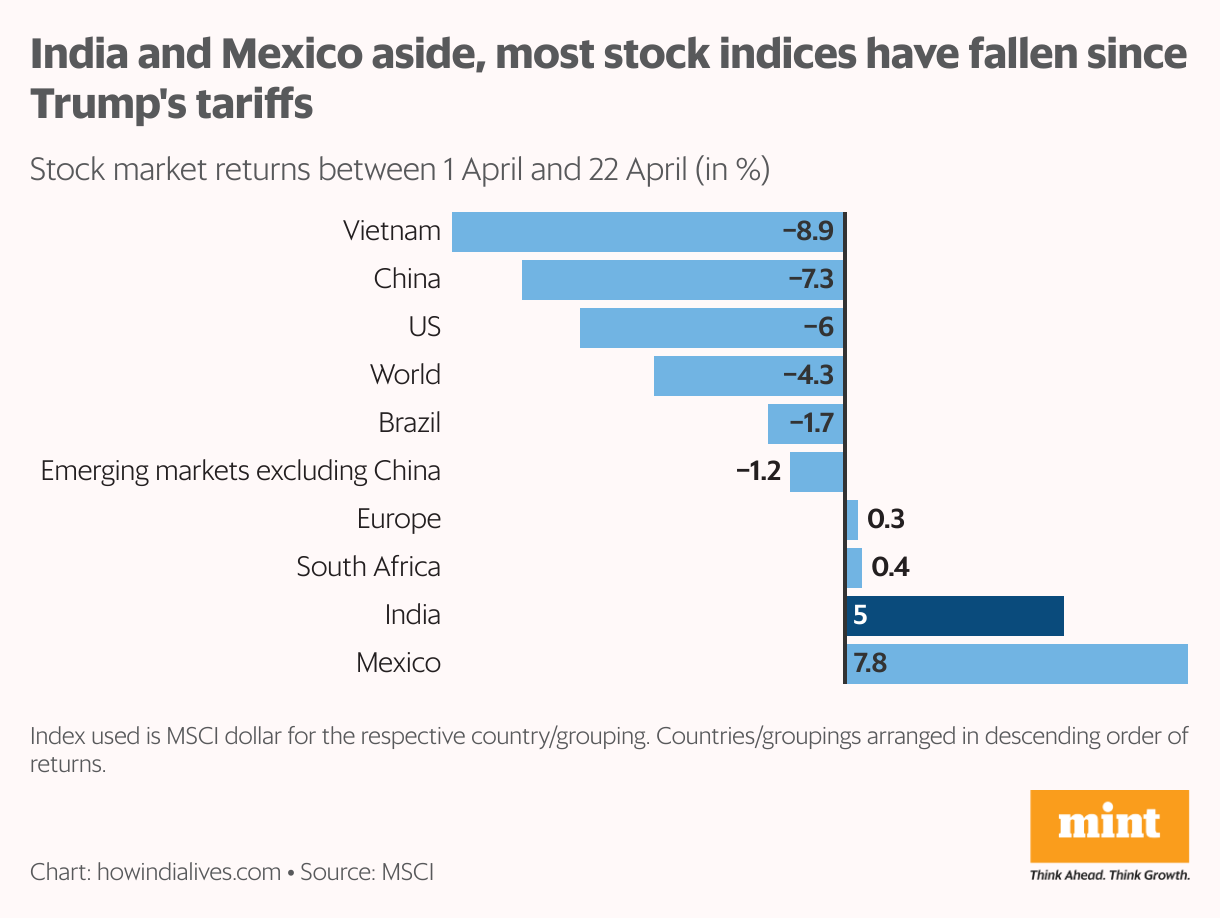

Stock returns for each country over 20 days since the eve of the Trump tariff announcements on 1 April show that equities globally were down. The quantum varied. The US and Chinese markets were down sharply. As was the case with the stock market in Vietnam, which has become an alternative to China for companies looking to site factories and supply to the US market. Overall, emerging markets, even excluding China, were down. On the other hand, some other markets, notably India and Mexico, which are seen as benefiting from the possible exit of companies from China, rose sharply.

Also Read | Mint Primer: What Trump’s tariff tantrums mean for investors

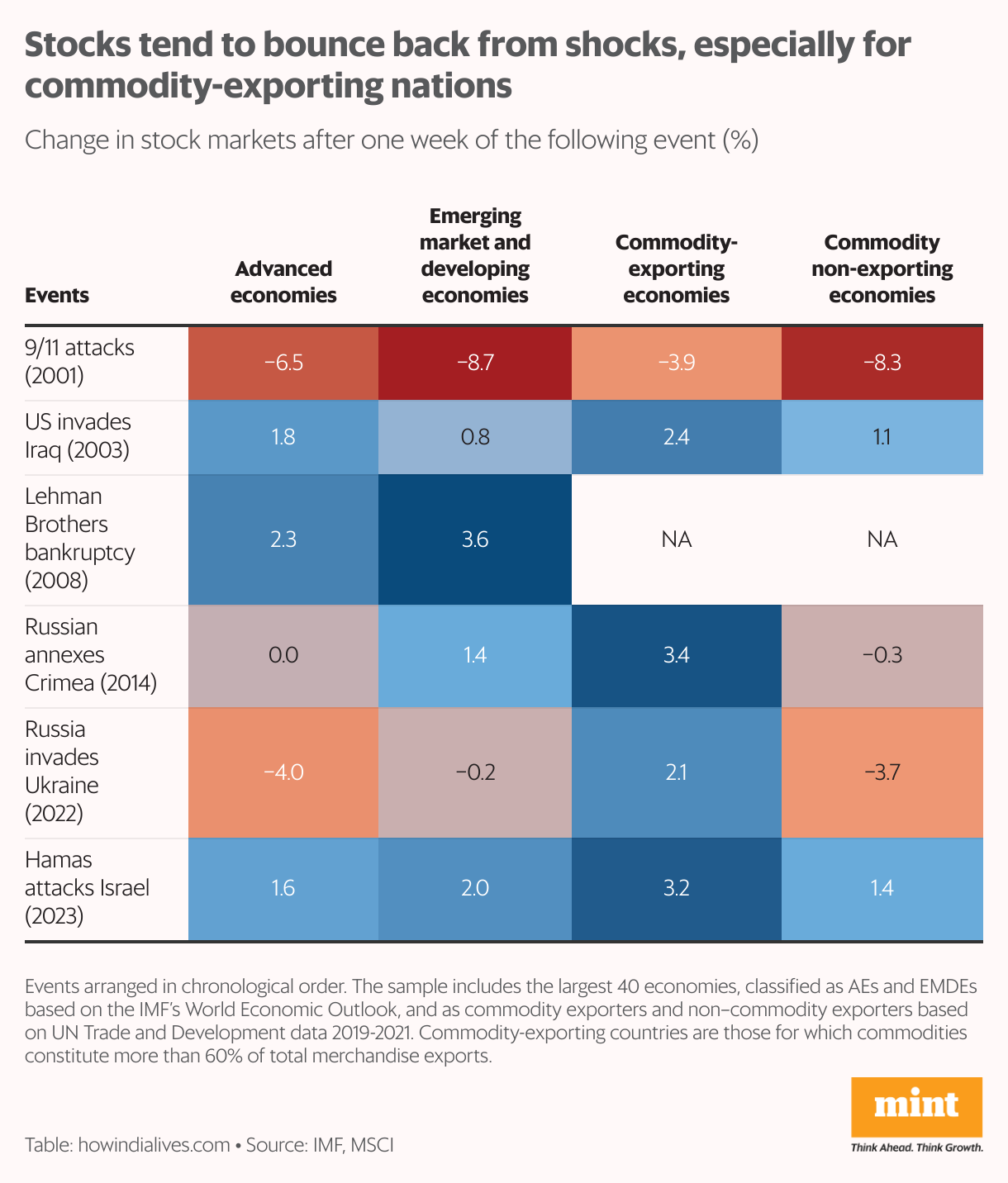

The IMF, in its latest Global Financial Stability Report, looked at how stocks reacted over the course of one week to major global geopolitical ‘shocks’ like the 9/11 attack and the Russian invasion of Ukraine. This shows that while markets fell, they bounced back. Stocks in commodity-exporting countries (such as the major oil exporters) saw the strongest bounce back within a week. Interestingly, both developed and emerging market stocks were up one week after the collapse of Lehman Brothers in 2008, driven in part by sharp interest rate cuts and massive liquidity infusions by central banks across the world.

Currency surprise

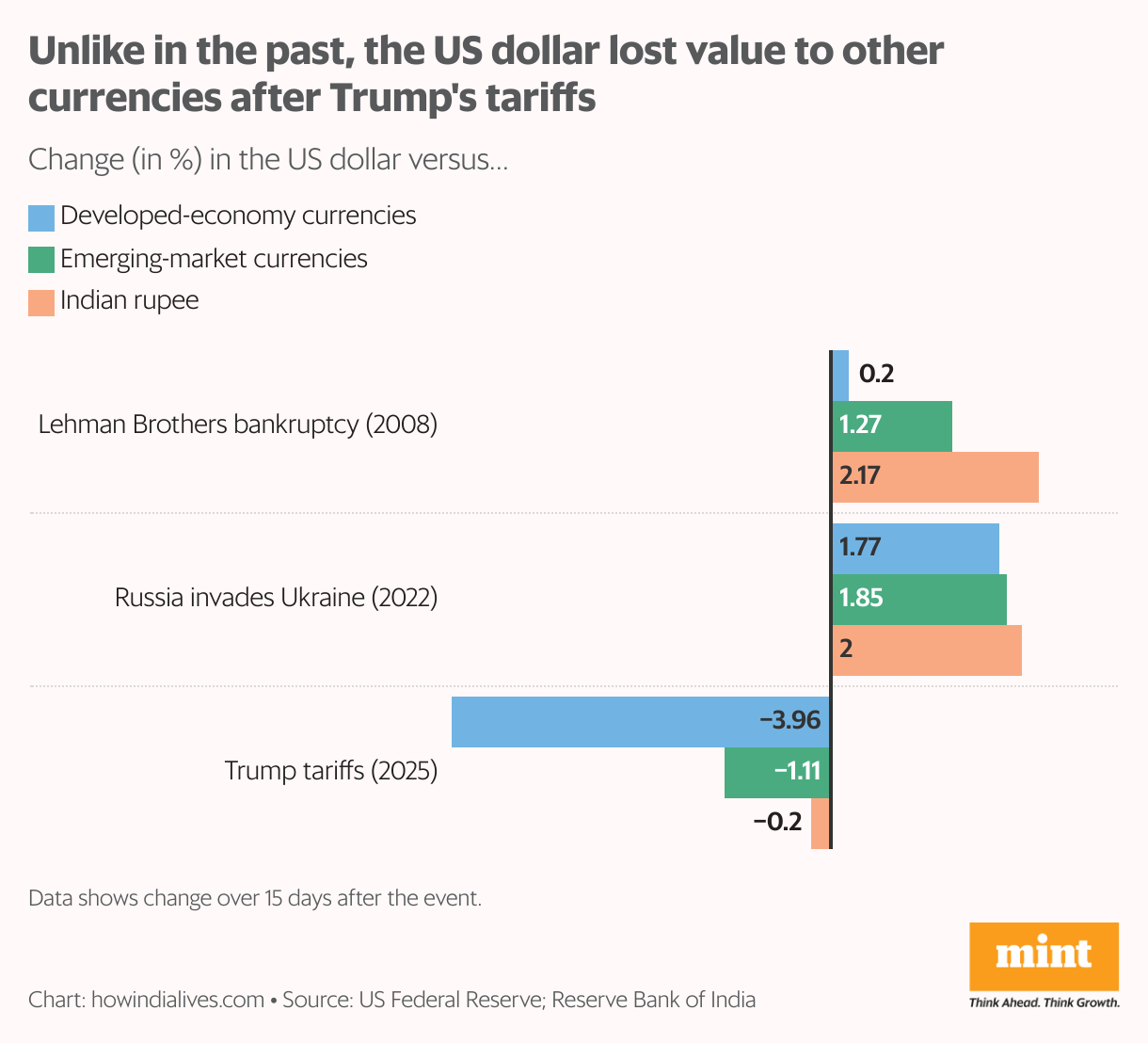

The Trump tariff crisis, at least in its immediate impact on markets, has been different in remarkable ways. A major difference in the reaction to the Trump tariff shock, as opposed to other shocks, was that investors no longer saw US financial instruments as safe havens. US treasuries, normally a go-to in times of uncertainty, saw a wave of selling, forcing yields up (bond prices and yields move in opposite directions).

When Russia invaded Ukraine, the US dollar rose against the rupee, as well as against currencies of most emerging and developed markets. Similarly, in 2008, in the aftermath of the greatest economic crisis since the Great Depression, the dollar strengthened against both developed-market and emerging-market currencies in the fortnight after the collapse of Lehman Brothers. In sharp contrast, the Trump tariffs saw the dollar remain flat against the rupee and lose value against developed-market currencies.

Dollar factor

Geopolitical and economic shocks are usually a double whammy for Indian markets. Firstly, there’s the impact on stocks. Secondly, if foreign investors sell stocks in India and pull money out, the rupee slides against the dollar. In each of four shock events over the past decade, over a 20-day period, dollar returns of the BSE Sensex have trailed its rupee returns by a substantial margin. That’s the currency effect, and the rupee is losing value against the dollar.

However, during the first Trump tariff shock in March 2018, when the US imposed tariffs on Indian steel and aluminium (and India responded with retaliatory tariffs in June), the dollar returns on the Sensex were about par with its rupee returns. In this round of Trump tariffs, imposed on 2 April, the Indian markets have risen in the three weeks since, with dollar returns of the BSE Sensex beating its rupee returns.

Also Read | Mint Primer: How will Trump’s next obsession, a weaker dollar, play out?

No safe haven

The biggest difference is how bond markets have reacted. Typically, the US treasury bond is a safe haven, especially during economic uncertainty. But the US treasury market took a beating. This was partly due to technical reasons (large holders of bonds unwinding leveraged trades), but it also reflected a new thinking among investors that US assets were no longer as secure as before.

In times of uncertainty, the cumulative change in the spread between Indian government bonds (10-year maturity) and the equivalent US treasury bond should widen, as investors dump emerging market assets and buy US treasuries. That’s what happened in the immediate aftermath of the Russian invasion of Ukraine. Amid Trump tariffs, the spread widened for two days, but then dramatically tightened. Ten days after the crisis, this spread has actually shrunk by a cumulative 25 basis points. By the standards of the gigantic US treasury market, that’s a massive move.

www.howindialives.com is a database and search engine for public data