The British Pound showed a mixed performance on Thursday after fresh survey data highlighted ongoing weakness in the UK construction sector, reinforcing concerns that higher energy costs and economic uncertainty are weighing on activity.

Pound to Euro (GBP/EUR): 1.15625 (-0.02%)

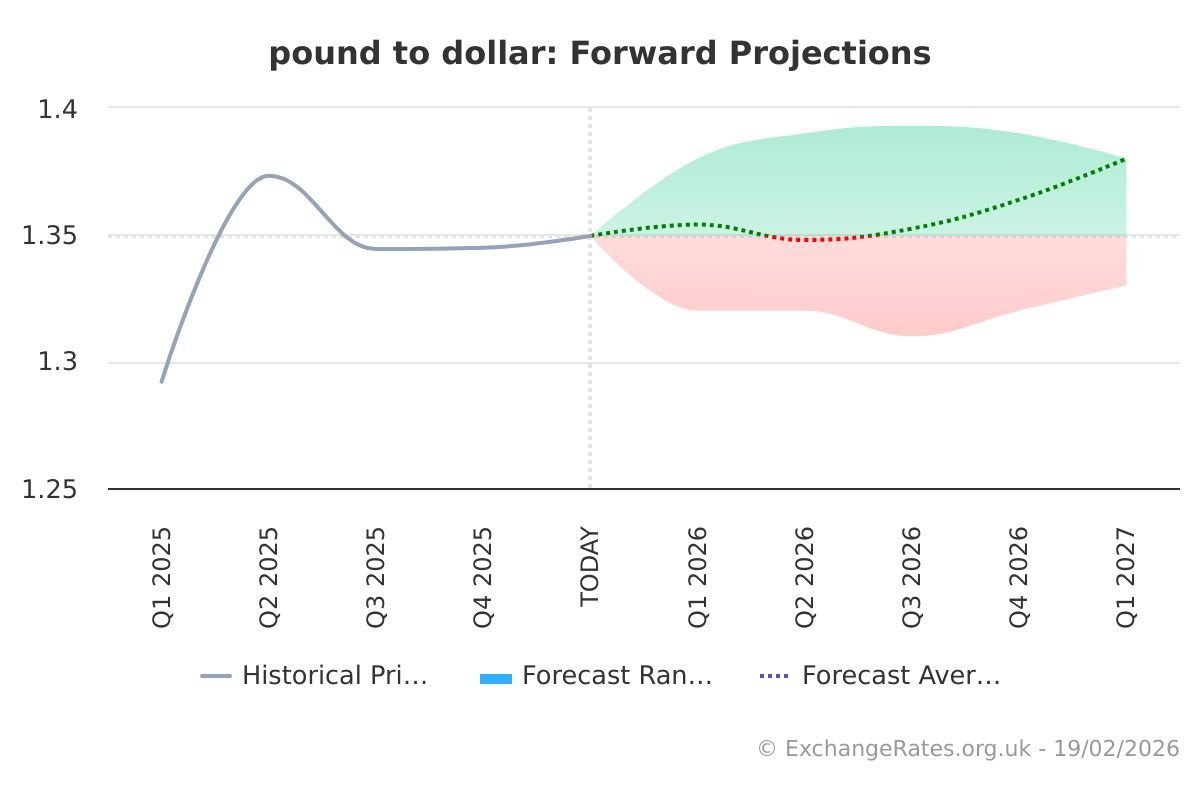

Pound to Dollar (GBP/USD): 1.34583 (+0.25%)

Euro to Dollar (EUR/USD): 1.16396 (+0.27%)

The latest S&P Global/CIPS Construction PMI fell to 38.2 in May, down from 39.7 in April and below market expectations of 40.5. The reading marks one of the weakest periods for the sector outside of the pandemic and Global Financial Crisis.

According to Pantheon Macroeconomics, the headline survey paints a very bleak picture, although economists caution that the PMI has recently understated actual construction activity.

“We take the construction PMI with a pinch of salt because it has been a poor predictor of construction output growth lately.”

Pantheon economists noted that the survey’s implied 3.0% three-month-on-three-month contraction in output would normally only be associated with a severe recession.

“The Construction PMI is at its lowest since the GFC, if we ignore the pandemic-related disruptions.”

Construction Outlook Remains Weak

While the survey may exaggerate the scale of the downturn, Pantheon believes activity is likely to remain under pressure until energy costs ease and uncertainty surrounding interest rates and UK politics diminishes.

“We think construction output will keep falling—if more modestly than the PMI suggests—until energy prices begin to fall back and there is more clarity over the interest rate and political outlook.”

Forward-looking indicators also deteriorated further. The future activity index fell to 53.0 from 57.9, while new orders dropped to 37.5, suggesting little immediate improvement ahead.

Housebuilding remained particularly weak, with the residential activity index slipping to 36.0, while commercial construction also deteriorated sharply.

Rising Costs Add to BoE Dilemma

One area likely to attract attention from Bank of England policymakers was the continued acceleration in cost pressures.

“The input price balance increased to 83.5, from 81.4, and the highest since June 2022.”

Pantheon noted that rising fuel costs are continuing to push construction expenses higher, with subcontractor charges also increasing rapidly.

The combination of weakening growth and rising costs highlights the difficult balancing act facing the Bank of England. While softer activity argues against higher rates, persistent inflation pressures continue to complicate the policy outlook.