The Indian Rupee has witnessed one of its most volatile periods in recent years, swinging from a record low to a strong recovery before coming under pressure once again. The currency’s journey has largely mirrored developments in the US-Iran conflict, which has driven sharp movements in global crude oil prices and investor sentiment. As India imports more than 85% of its crude oil requirements, every major move in oil prices directly affects the Rupee, inflation, trade balances, and the broader economy.

Why the Rupee Matters

A weaker Rupee increases the cost of imports, especially crude oil, making fuel more expensive and adding inflationary pressure across the economy. Higher import costs widen India’s trade and current account deficits, while foreign investors often reduce exposure to emerging markets during periods of uncertainty, putting additional pressure on the currency.

On the other hand, a stronger Rupee lowers imported inflation, reduces India’s oil import bill, and gives the Reserve Bank of India (RBI) greater flexibility in managing interest rates without worrying about rising prices.

Throughout 2026, the Rupee has experienced both extremes, with geopolitical tensions remaining the biggest driver.

How the Rupee Fell to a Record Low

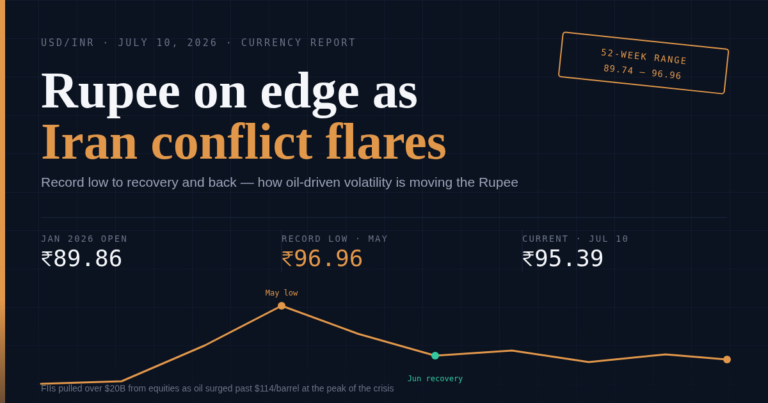

The Rupee began 2026 trading around ₹89.86 per US Dollar.

The turning point came in late February when the United States entered into direct conflict with Iran. The closure of the Strait of Hormuz, through which nearly 20% of global oil supplies pass, triggered fears of major supply disruptions.

Crude oil prices surged from below $80 per barrel to above $114 per barrel, significantly increasing India’s annual crude import bill by more than $60 billion compared to pre-war levels.

The higher import bill widened India’s current account deficit, while foreign institutional investors (FIIs) withdrew more than $20 billion from Indian equities during the first four months of the year, exceeding the total outflows recorded during the previous year.

The combination of rising oil prices, heavy foreign fund outflows, and a stronger US Dollar pushed the Rupee to an all-time low of ₹96.96 per Dollar in mid-May.

Although the RBI intervened by selling US Dollars through state-run banks, these measures slowed the decline rather than reversing it.

The Rupee’s Recovery

Market sentiment improved after the United States and Iran agreed to a temporary two-week ceasefire and discussions began to reopen the Strait of Hormuz.

The easing of supply concerns caused Brent crude prices to fall by roughly 16%, bringing prices back to around $92-94 per barrel.

Lower oil prices immediately reduced pressure on India’s import bill and helped improve investor confidence.

The RBI further supported the recovery by announcing several measures aimed at attracting foreign currency inflows, including subsidised hedging facilities for foreign currency deposits and external commercial borrowings.

These measures resulted in a sharp increase in corporate hedging activity.

- Exporters booked a record $46.3 billion in foreign exchange hedges during June, up 45% year-on-year.

- Importers added nearly $74 billion in hedging positions.

- Total corporate foreign exchange hedging reached a record $120 billion during the month.

Supported by lower crude prices and improved capital flows, the Rupee strengthened from its record low of ₹96.96 to around ₹94.50 per Dollar, posting its first quarterly gain in five quarters.

Despite the recovery, analysts noted that the RBI remained focused on rebuilding India’s foreign exchange reserves, which had fallen from a peak of $728.5 billion in March to $681.6 billion.

At the same time, the RBI’s short-Dollar forward position had expanded to nearly $110 billion, limiting the scope for further appreciation in the Rupee.

Renewed Pressure After Ceasefire Collapse

The recovery proved short-lived.

On July 8, Iran attacked three commercial vessels passing through the Strait of Hormuz, prompting fresh US military strikes.

During the NATO Summit in Ankara, US President Donald Trump declared that the temporary agreement with Iran was effectively over.

The renewed conflict pushed crude oil prices higher once again.

- West Texas Intermediate (WTI) crude rose by more than 4%.

- Brent crude increased 5.2% during the session, settling at $78.02 per barrel.

The Rupee weakened sharply, closing at ₹95.56 per Dollar, nearly 60 paise weaker than the previous session’s close of ₹94.97.

Indian equity markets also reacted negatively.

- The Sensex fell 2.15%.

- India VIX, often referred to as the market’s fear gauge, surged nearly 30% to 15.08, reflecting a sharp rise in market uncertainty.

Reports also suggested that India was exploring diplomatic options to ensure safe passage for multiple oil tankers waiting in the Persian Gulf.

Where the Rupee Stands Today

As of July 10, the Rupee is expected to open around ₹95.32-95.35 per Dollar, after closing at ₹95.3875 on Thursday.

The currency has traded within a range of ₹94.96 to ₹95.60 this week as markets continue to react to developments in the US-Iran conflict.

Brent crude has remained volatile, fluctuating between $71 and $80.50 per barrel, and was last trading near $76.34, about 2% lower on Thursday.

Market participants continue to report Dollar selling by state-run banks, indicating ongoing RBI intervention to prevent excessive weakness in the Rupee.

Analysts believe expectations of a prolonged depreciation have moderated, although RBI purchases of foreign exchange to rebuild reserves could limit any significant appreciation.

Exporters are expected to continue hedging selectively, while importers are likely to increase Dollar buying whenever the Rupee strengthens.

The Road Ahead

Several key developments are expected to determine the Rupee’s direction in the coming weeks.

The biggest immediate risk remains the ongoing US-Iran conflict. Any further escalation over the weekend could once again push crude oil prices higher and increase pressure on the Indian currency.

Investors will also closely monitor the US Federal Reserve’s July policy meeting, as any change in US interest rates could influence global capital flows into emerging markets such as India.

Crude oil prices remain another critical factor. A sustained decline in Brent crude below $80, and especially below $75 per barrel, would significantly reduce India’s import bill, narrow the current account deficit, and provide greater flexibility for the RBI.

Finally, record corporate hedging activity of $120 billion during June suggests that businesses are increasingly preparing for a prolonged period of currency volatility. While stronger hedging improves risk management, it could also amplify short-term movements in the Rupee as importers and exporters actively manage their foreign exchange exposure.

The USD/INR pair has traded within a 52-week range of ₹89.74 to ₹96.96. After testing both ends of that range over the past four months, the Rupee’s next major move will largely depend on whether geopolitical tensions ease or whether the conflict enters another phase of escalation.

Disclaimer – The stock/s and indices mentioned in this article is discussed solely for informational and educational purposes. It should not be construed as investment advice or a recommendation to buy or sell any securities. Investors should conduct their own research or consult a financial advisor before making any investment decisions. Investments in securities market are subject to market risks. Read all the related documents carefully before investing.