European currencies have held up relatively well amid U.S. dollar strength. That may be ending.

- The U.S. dollar has enjoyed its best two weeks in 20 months.

- European currencies have fared better than their APAC counterparts.

- U.K. CPI data may break British pound resilience.

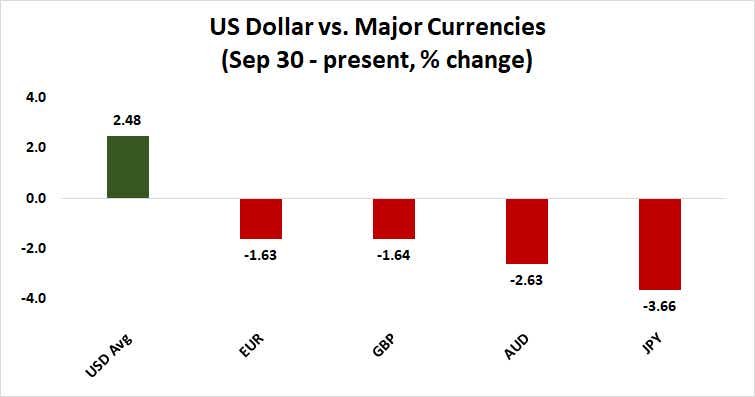

The U.S. dollar launched a forceful push higher this month, adding 2.2% against an average of its major counterparts in the first two weeks. It marked the strongest such run since February 2023. European currencies have fared a bit better than their Asia Pacific peers against this backdrop. They now look vulnerable to catch-up losses.

The British pound and the euro shed just over 1.6% each as the greenback roared back to life. That compares well with a loss of 2.6% for the Australian dollar and 3.7% for the Japanese yen. It might also leave room for a deeper slide amid a dovish shift in monetary policy expectations for European central banks.

As the U.S. dollar jumps, European currencies are outperforming

Policy expectations for the Bank of Japan (BOJ) and the Reserve Bank of Australia (RBA) have been relatively stable, making the outsized drop in their currencies appear to be mostly driven by a rebound in U.S. yields. Meanwhile, traders trimmed back the expected scope for European Central Bank (ECB) and Bank of England (BOE) rate cuts.

This helped to insulate European currencies from the worst of the dollar’s offensive. Incoming news may force a rethink. First up is September’s U.K. consumer price index (CPI) report. It is expected to show that headline inflation cooled to 1.9% year-on-year last month, the lowest since April 2021. An ECB policy update is due later in the week.

As it stands, the markets are pricing in 35 basis points (bps) in interest rate cuts before year-end. That amounts to at least one standard-sized 25bps reduction and a 70% probability of getting 50bps in total at the remaining policy meetings in November and December.

The British pound may fall after U.K. CPI inflation data

U.K. economic data outcomes have deteriorated relative to baseline forecasts recently, according to analytics from Citigroup. A disappointing slowdown in the pace of service sector activity growth that translated into weaker-than-expected overall performance in September’s purchasing managers’ index (PMI) data is a case in point.

Meanwhile, August’s U.K. CPI data showed that the lion’s share of sticky inflationary pressure remains concentrated in the recreation and hospitality sectors for a fifth consecutive month. These areas’ reliance on discretionary spending makes them cyclically vulnerable. If the economy is decelerating, price pressures there ought to ease.

All of this might come together to produce the kind of CPI report that encourages a dovish reevaluation of BOE policy expectations. Even a modest shift to lock in 50bps in cuts this year might be enough to inspire a key breakdown for the British pound as it rests squarely atop key price support at 1.30 against the U.S. dollar.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.