Last week, the Reserve Bank of India (RBI) transferred a record dividend of Rs 2.87 lakh crore to the Centre for 2025-26. Unlike companies that transfer a portion of their profits to shareholders, the RBI must hand over its entire gain to the government. But how did it end up generating such a big profit?

First and foremost, the RBI’s objective is not to make a profit; it just so happens that the actions it must take to achieve its objectives — ensuring adequate supply of money (liquidity) in the banking system, appropriately investing its foreign exchange reserves, and maintaining order in the bond and foreign exchange market — result in a lot of revenue.

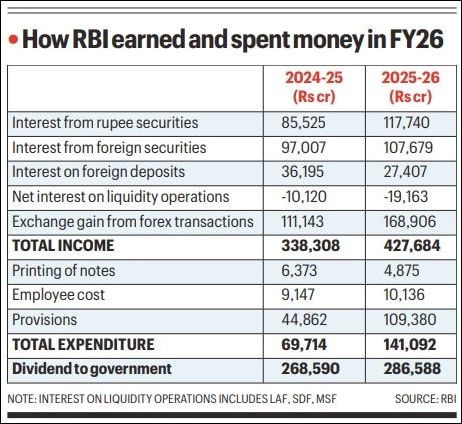

In 2025-26, the RBI’s total income was a record Rs 4.28 lakh crore, up 26% from the previous year. Of this, it spent about a third, or Rs 1.41 lakh crore. But how did the RBI earn so much and what did it spend on?

Supporting the rupee

Last year was highly turbulent: tariffs, wars, and the AI boom led to foreign investors dumping Indian shares and debt, while India’s gold and silver import bill hit new highs. This led to the rupee falling by 10% against the US dollar. The byproduct of the RBI’s attempts to defend the rupee was the largest income stream for the central bank.

The RBI shores up the rupee by selling previously-bought foreign currency. The difference in cost and selling price represents a pure profit. For instance, if a dollar was bought for 75 rupees and sold at 95, that’s a profit of Rs 20. All in all, the RBI sold $195 billion of foreign currency on a gross basis in 2025-26.

This led to what is called an ‘exchange gain from foreign exchange transactions’ of Rs 1.69 lakh crore, 52% higher from 2024-25.

The RBI does not disclose the average historical cost of the foreign currency it holds or sells.

Consequences of rupee defence

Story continues below this ad

Selling forex has consequences which the RBI must negate. And these actions generate more income.

When the RBI sells dollars, it gets rupees in return. This reduces the availability of Indian rupees — or, rupee liquidity. Unaddressed, this rupee liquidity shortage would raise market interest rates.

In 2025-26, the RBI did not want interest rates to rise (it cut the repo rate by 125 basis points). So, it had to infuse rupees into the Indian market to nullify the impact of its dollar sales. It did so by buying central government bonds worth nearly Rs 9 lakh crore from those who hold them – banks, for instance. These bonds, and those it already held, provided an interest of Rs 1.18 lakh crore to the RBI last year.

While these government bond purchases infuse long-term liquidity, short-term mismatches require the RBI to lend and hold banks’ money. On the whole, these short-term operations saw the central bank pay out Rs 19,163 crore as interest.

Story continues below this ad

The RBI also earns interest on the foreign securities it holds as part of its foreign exchange reserves. In 2025-26, this interest income rose 11% to Rs 1.08 lakh crore. It also received Rs 27,407 crore as interest on its foreign deposits.

Cost of operations

Two expenditure items are straightforward but minor in the overall scheme of things. Printing of new currency set back the RBI Rs 4,875 crore, while employee cost rose 11% to Rs 10,136 crore.

The big chunky expenditure was provisions. Like any other bank, the RBI must set aside money if its loans — in the RBI’s case, investments — are doing poorly. This happens when the value of its holding of domestic and foreign securities falls due to a rise in yields, which is what happened in 2025-26.

Money also had to be set aside for the losses being incurred by the RBI on its forward contracts — another instrument used to defend the rupee last year. All put together, the net provision made by the RBI on account of these three issues was a massive Rs 1.09 lakh crore.

Story continues below this ad

The provision would have been higher had the Contingent Risk Buffer not been cut to 6.5% of the balance sheet from 7.5%.