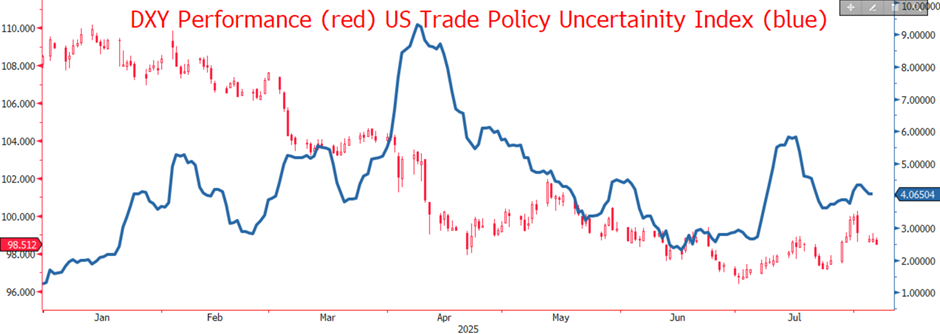

When Trump first started making serious noises regarding his tariff agenda, back when he was just President Elect, it was a one way bullish USD street. Then, that narrative was inverted, with Trump’s relentless put-offs and erratic announcements sending the once unstoppable USD rally spiraling downwards.

But as Trump has ran out of road to delay and has had to actually enforce his rhetoric with policy, the story has become somewhat more complex. We saw this most recently as Trump did actually implement a variety of tariffs, not quite as high as first threatened, but real this time, making all the difference.

15% on the EU, 15% on Japan, a whopping 41% on the South East Asian nation of Laos and all of a sudden all the bluster has become material. And with that, USD caught some winds in its sales.

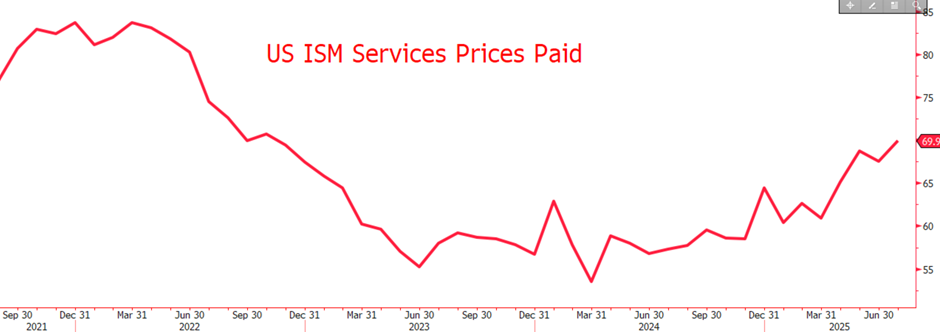

Almost as if one cue, ISM PMI data released, showing the service sector putting out a below expectations performance in July. More interesting however, was the prices paid data, showing that even though there are now tariffs on services, the highest rate of price inflation since 2022.

Powell and the market at large had sounded the alarms regarding the potential inflationary impact tariffs could have on the United States, with Powell going as far as to suggest that September would be likely when prices start inching upwards.

Almost like prophecy, the first tender sign of such behaviour has arisen, whether this is simply a slip, or the beginning of a slide remains to be seen. It could mark a slight return to the old Dollar bullish tariff narrative, higher tariffs higher inflation, stronger Dollar, explaining the most recent tariff fueled Dollar bump. But with Trump pledging to select a new Fed Chair by the end of the week, one who seems likely to be aggressively dovish in their approach, things could get out of hand very quickly.