Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

Global rally loses steam

The monster rally that has defined global markets for the last three weeks lost momentum overnight as concerns around the inflationary impact of the US port strike and growing tensions in the Middle East hit sentiment.

In the US, east-coast port workers commenced a strike at midnight on Tuesday (EDT) that sparked fears that supply issues could drive a renewed spike inflation.

In the Middle East, a series of missile strikes on Isreal, launched from Iran, caused markets to worry about potential escalation.

The US’s S&P 500 fell 0.9% as it turned from all-time highs. The Dow Jones fell 0.4% while the tech-focused Nasdaq lost 1.5%.

In FX markets, the safe-haven US dollar saw big gains, with the USD index up 0.4% as it hit two-week highs.

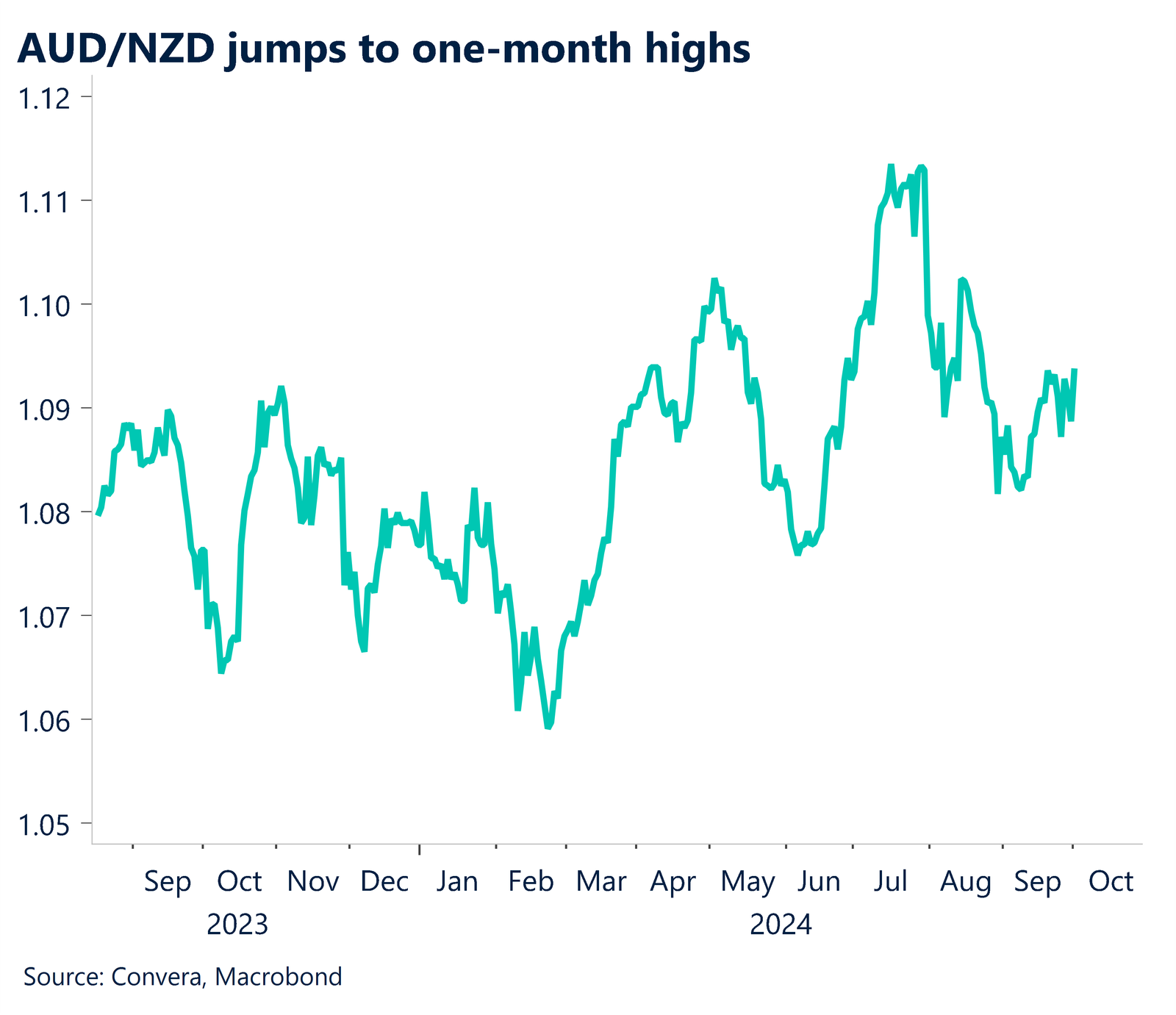

The AUD/USD fell 0.5% while NZD/USD led losses, down 1.0%. The AUD/NZD hit one-month highs.

In Asia, the USD/SGD and USD/CNH both climbed 0.3%.

AUD/EUR at 16-month highs after CPI drop

The euro was weaker across markets after Eurozone inflation fell from 2.2% in August to 1.8% in September.

The euro fell in most markets but, most notably, saw the AUD/EUR hit 16-month highs.

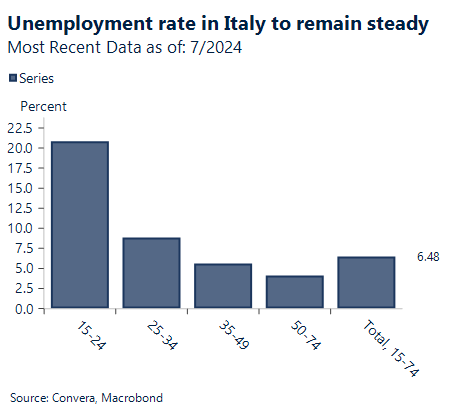

Looking forward, Italy’s 6.5% unemployment rate looks likely remain steady. August saw a decline in composite PMI employment, despite a sharp increase in the ISTAT services employment index. For now, the EUR/USD is supported by the 1.10 handle, but a break lower might trigger further euro losses

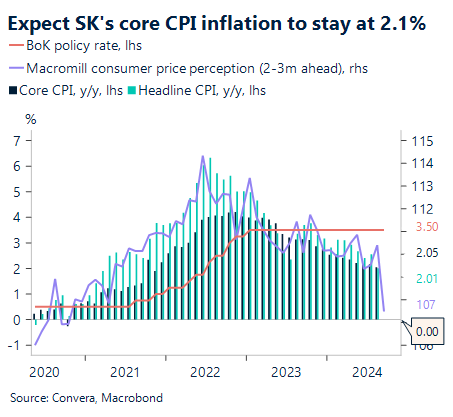

Korean won watches for inflation trends

Because of the decline in oil prices, we anticipate that inflation will drop from 2.0% in October to 1.9% y-o-y in September.

However, core inflation looks likely to stay at 2.1% in September due to the modest increases in prices outside of food and energy.

The inflation outlook would be more vulnerable if our projection came to pass, which would put more pressure on the BOK to lower interest rates at the next policy meeting in October.

We anticipate inflation to decelerate to below 2% by the end of 2024 due to weak domestic demand and diminishing supply-side pricing pressures, which should allow for additional rate cuts beyond 2024.

In comparison to its other Asian rivals, Won’s performance has been somewhat subdued despite the Fed’s pivot.

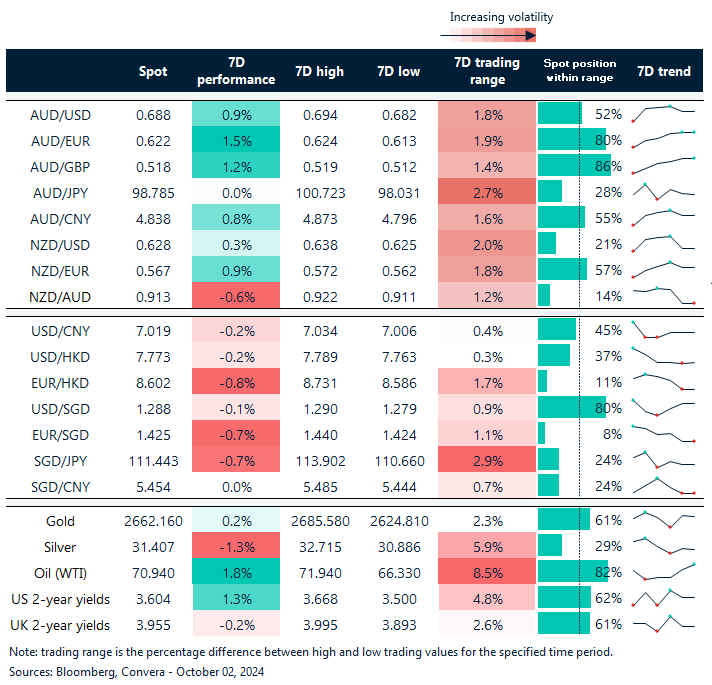

USD extends comeback as global markets turn lower

Table: seven-day rolling currency trends and trading ranges

Key global risk events

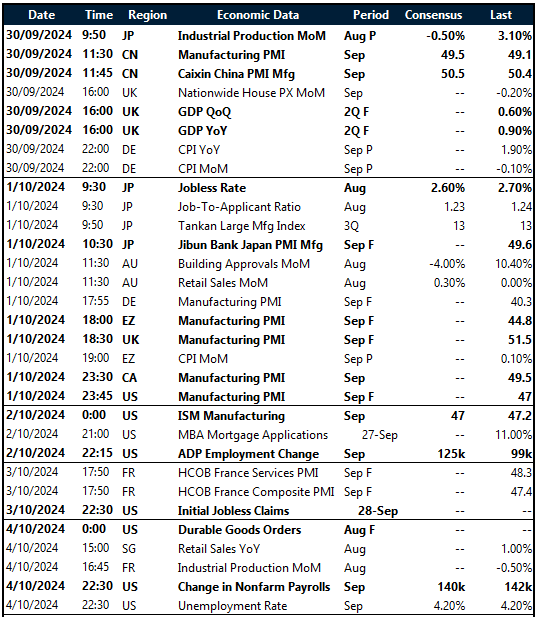

Calendar: 30 September – 4 October

All times AEST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.