Written by Convera’s Market Insights team

Downside risk on the cards for CAD

Ruta Prieskienyte – Lead FX Strategist

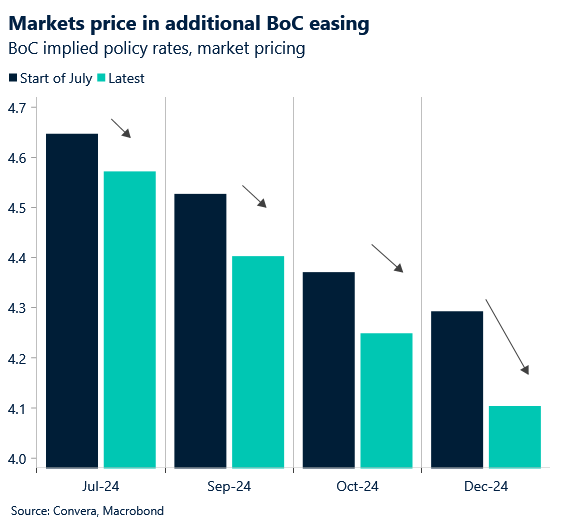

The Canadian dollar weakened to a 2-week low towards C$1.37 against the US dollar as it continues to face pressure following the weekend’s assassination attempt on former President Donald Trump. Domestically, the BoC Business Outlook Survey underscored continued pessimism among Canadian firms, attributing it to weak sales expectations and high equipment costs that deter investment.

Attention now turns to the forthcoming release of Canada’s CPI data, the crucial release ahead of the July BoC rate decision in just over a week. The market participants are anticipating the headline CPI to slow from 2.9% to 2.7% YoY, the median core measure from 2.8% to 2.7% and the trim core measure from 2.9% to 2.8%. If this were to materialize, it would support the case for a back-to-back cut in July given the rising unemployment rate in the month prior. There are already 20bp in the price for a July cut and if inflation were to move in line with expectations, we could see markets price in additional easing for next week, leaving CAD in a vulnerable position.

Opposing forces still in motion

George Vessey – Lead FX Strategist

Two opposing forces (fiscal- and monetary policy) are still keeping FX and fixed income traders on their feet. Politics continues to put upward pressure on yields and the US dollar, while the expected easing cycle by the Federal Reserve (Fed) might do the opposite. US macro data this week is, as ever, eagerly awaited, but we think risks are quite balanced for the dollar given the political backdrop.

PredictIt odds that Donald Trump wins a second term as president have risen to about 67%, from 60% beforehand, after the assassination attempt on the former president over the weekend. So far the market reaction has been fairly muted, but the yield on 30-year Treasuries surpassed the rate on two-year notes for the first time since January on bets Trump’s policies will spur growth. Markets are grappling with the concept of the “Trump Trade,” which reflects the expectation of a pro-business environment and a significant boost to the US economy through fiscal stimulus, which might limit the scale of rate cuts by the Fed, helping the dollar maintain its high growth and high yield advantage. Nevertheless, we suspect US macro could be a bigger driver of the FX market through the summer. With recent data pointing to easing inflation, a cooling labour market and moderating consumer spending, concerns about an abrupt US slowdown and a more dovish Fed may weigh heavier on the dollar.

Indeed, softer data in recent weeks, including broad-based weakness in the June CPI, have raised the probability of two Fed rate cuts this year. Moreover, yesterday’s modest decline in manufacturing conditions in the New York Fed’s Empire State Manufacturing Survey suggests the ISM Manufacturing PMI for July could soften modestly as well. Today, US retail sales are in focus and will likely show a third straight month of weak spending amid high borrowing costs and a cooling labour market.

Euro tests a four-month high

Ruta Prieskienyte – Lead FX Strategist

A risk off sentiment succumbed the markets following disappointing economic data from China and the assassination attempt on Donald Trump. European equities and bonds were down at the start of the week, but the euro emerged victorious in an otherwise quiet session. EUR/USD claimed a fourth consecutive session of gains to rise to its highest level since the end of March.

In terms of domestic developments, the Eurozone industrial production surprised to the upside, falling 0.6% m/m in May versus the market consensus of a 1% decline. Elsewhere, France was yet again under pressure as auditor slammed its plans to fix the gaping hole in the country’s finances. President Macron’s outgoing administration pledged new spending cuts and revenue-boosting measures in April to get back on course with derailed plans to bring the budget deficit within 3% of economic output in 2027. However, the state auditors see those plans as noncredible and unrealistic given they are based on a whole host of particularly optimistic set of assumptions. The review is another red flag for the euro area’s second-largest economy, whose next government will need to find more than €15 billion in extra revenue or savings a year to meet European Union demands.

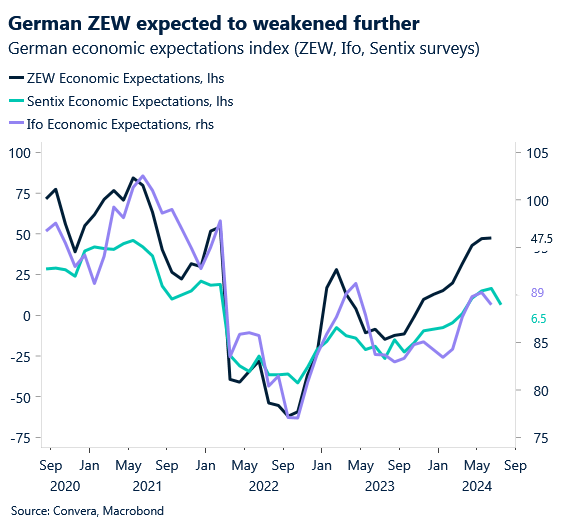

Today’s German ZEW index will be the highlight of the week from the domestic calendar and is expected to show a further loss of momentum in leading activity indicators. This may take some of the steam out of the bullish momentum, especially with the daily EUR/USD relative strength index steadily approaching overbought territory. Despite that, $1.09 could be the target in the short term. We will also be closely monitoring the ECB’s bank lending survey due later today, which will provide an update on the tightening effect on eurozone credit supply.

US yields on holding near lows

Table: 7-day currency trends and trading ranges

Key global risk events

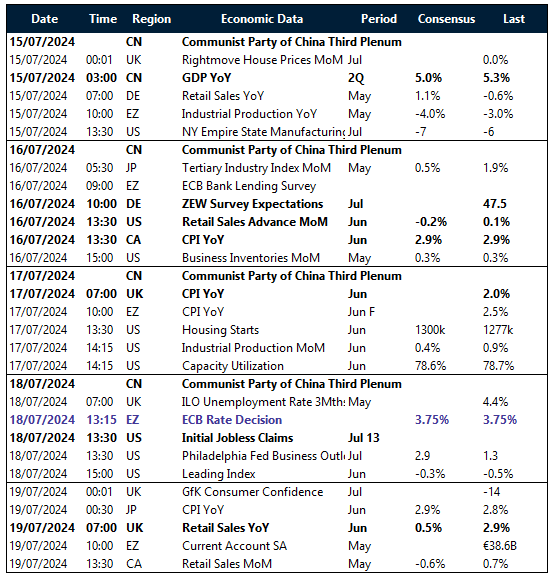

Calendar: July 15-19

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.