- The Pound Sterling failed another attempt above 1.3400 versus the US Dollar.

- The Fed and the BoE stuck to their cautious rhetoric amid US tariff uncertainties.

- Technicals show that bullish potential remains intact for the pair whilst above 1.3165.

The Pound Sterling (GBP) erased weekly gains versus the US Dollar (USD) after the GBP/USD pair breached the critical 1.3290 support.

Pound Sterling wilted as the King Dollar regained poise

The bearish momentum around the GBP/USD pair regained traction in the second half of the week as demand for the US Dollar re-emerged following a weak start.

The Greenback remained on the defensive against its currency rivals ahead of the US Federal Reserve (Fed) policy announcements. Despite US President Donald Trump stating last weekend that he would lower tariffs on Chinese imports ‘at some point’, uncertainty remained high over a thaw in US-Sino trade relations.

Additionally, doubts over a potential US-Japan trade deal intensified after Japanese Finance Minister Katsunobu Kato walked back comments made last Friday that seemed to suggest Japan might threaten selling some of its Treasury holdings as part of trade negotiations with the White House.

Fresh questions lingering on the trade front revived the USD’s downside in the early part of the week, allowing GBP/USD to briefly challenge the 1.3400 threshold again. However, the tide turned in favor of the US currency after the Fed kept the federal funds rate unchanged in the range of 4.25% to 4.50% on Wednesday, maintaining a cautious stance on the policy outlook. The Fed’s policy statement read that risks of higher inflation and unemployment had risen, further clouding the US economic outlook.

However, the Fed’s concerns over the heightened economic uncertainties in the face of Trump’s erratic trade policies were offset by renewed optimism surrounding potential US trade deals with some of its major trading partners.

The USD climbed to fresh monthly highs across the board after risk sentiment received a boost on the announcement of a “breakthrough deal” by US President Trump and British Prime Minister Keir Starmer on Thursday.

The US-UK trade deal raised hopes that US trade agreements with other countries are in the offing, especially as the US and China begin their first high-level trade talks in Switzerland on Saturday. US Treasury Secretary Scott Bessent and Chief Trade Negotiator Jamieson Greer will meet with China’s Vice Premier, He Lifeng, over the weekend.

The pair tumbled to three-week lows below 1.3250 in the aftermath, unable to capitalize on the Bank of England’s (BoE) communication to maintain a gradual and cautious approach towards further easing.

The UK central bank lowered the Bank Rate by 25 basis points (bps) on Thursday as widely anticipated. However, five Monetary Policy Committee (MPC) members voted to cut rates by 25 bps, two members favoured a 50 bps reduction (Dhingra and Taylor), and two members voted to keep rates unchanged (Mann and Pill).

Heading into the weekend, the USD stood tall as elevated geopolitical risks in the Middle East, and between India and Pakistan, drove safe-haven flows into the buck, leaving the pair mired in multi-week troughs.

Week ahead: Trade updates and US/UK data on tap

With the Fed and BoE monetary policy decisions out of the way, attention shifts back toward the high-impact economic data releases from both sides of the Atlantic as an eventful week unfolds.

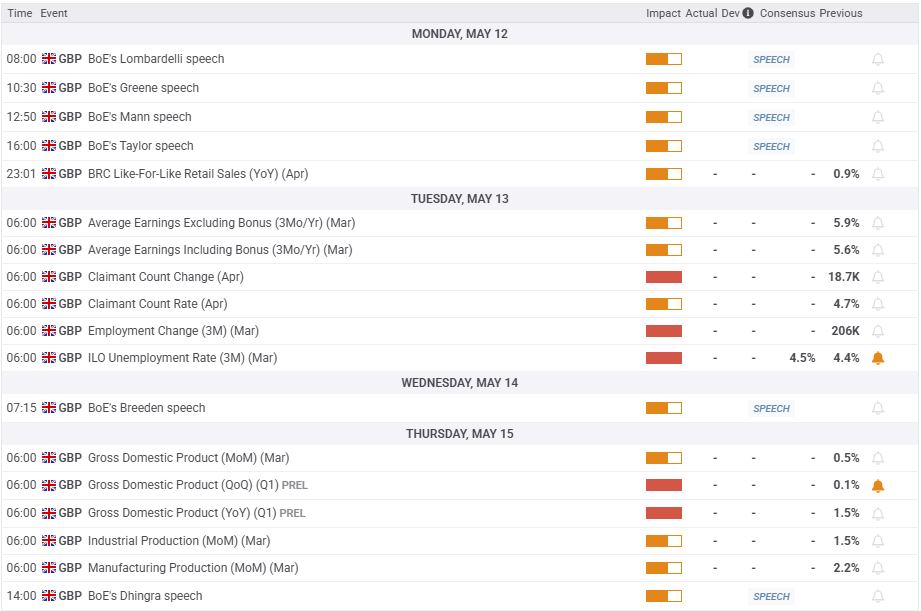

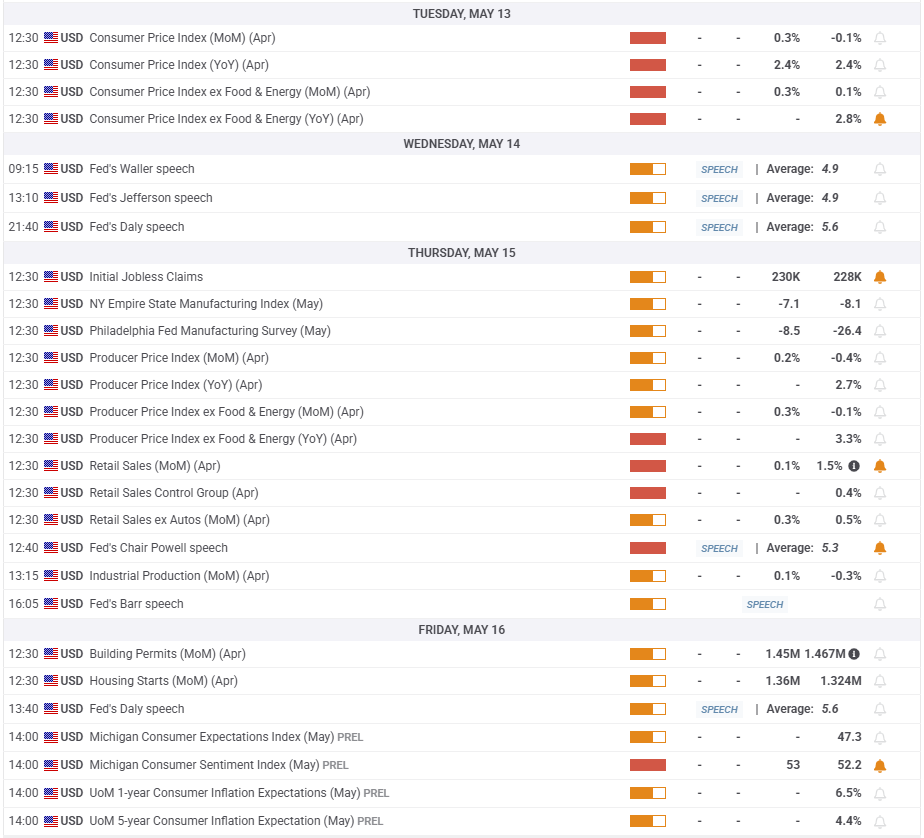

Monday is a quiet day in terms of macro releases, as investors prepare for Tuesday’s US Consumer Price Index (CPI) data. Ahead of the US inflation test, the UK labor data will provide some trading incentives to Pound Sterling traders.

It’s another data-dry docket on Wednesday, shifting the attention to the UK’s preliminary Gross Domestic Product (GDP) for the first quarter due on Thursday. Later that day, the US Producer Price Index (PPI) inflation data and the weekly Jobless Claims data will also entertain traders.

On Friday, only the preliminary University of Michigan (UoM) Consumer Sentiment and Inflation Expectations data will be noteworthy.

Apart from the economic statistics, potential trade deals between the US and its major trading partners and developments on the tariff front will continue playing a pivotal role in the week ahead.

Speeches from Fed and BoE policymakers will be closely scrutinized on fresh hints on the central banks’ policy outlooks.

GBP/USD: Technical Outlook

The daily chart shows that the 14-day Relative Strength Index (RSI) has eased its descent, currently trading near 52, indicating that dip-buying could emerge.

However, buyers remain cautious as the pair closed Thursday below the critical short-term 21-day Simple Moving Average (SMA) support at 1.3290.

Recapturing the latter on a weekly closing basis is required to revive the uptrend toward the three-year high of 1.3445.

Ahead of that, the 1.3400 mark will offer stiff resistance. If buyers regain control and overcome the aforementioned hurdles, the next target will be the February 2022 high of 1.3644.

If the selling pressure remains unabated, the 1.3200 round level will be initially tested, below which the 50-day SMA at 1.3072 will be threatened.

The line in sand for buyers is aligned at the 1.3000 psychological level.

Tariffs FAQs

Tariffs are customs duties levied on certain merchandise imports or a category of products. Tariffs are designed to help local producers and manufacturers be more competitive in the market by providing a price advantage over similar goods that can be imported. Tariffs are widely used as tools of protectionism, along with trade barriers and import quotas.

Although tariffs and taxes both generate government revenue to fund public goods and services, they have several distinctions. Tariffs are prepaid at the port of entry, while taxes are paid at the time of purchase. Taxes are imposed on individual taxpayers and businesses, while tariffs are paid by importers.

There are two schools of thought among economists regarding the usage of tariffs. While some argue that tariffs are necessary to protect domestic industries and address trade imbalances, others see them as a harmful tool that could potentially drive prices higher over the long term and lead to a damaging trade war by encouraging tit-for-tat tariffs.

During the run-up to the presidential election in November 2024, Donald Trump made it clear that he intends to use tariffs to support the US economy and American producers. In 2024, Mexico, China and Canada accounted for 42% of total US imports. In this period, Mexico stood out as the top exporter with $466.6 billion, according to the US Census Bureau. Hence, Trump wants to focus on these three nations when imposing tariffs. He also plans to use the revenue generated through tariffs to lower personal income taxes.