The Euro’s slide against the Pound has now consumed seven of the last eight trading sessions, and the reflex explanation of a soft single currency gets the attribution backwards. Sterling has done most of the work here: the Pound just closed out its best week in three months, printed a one-year high against the Euro, and managed both midway through a leadership transition with no confirmed Prime Minister and no named finance minister. The cross is falling because the Pound is being repriced upward, not because the Euro is falling apart.

A Bank of England hike went from coin flip to certainty in three sessions

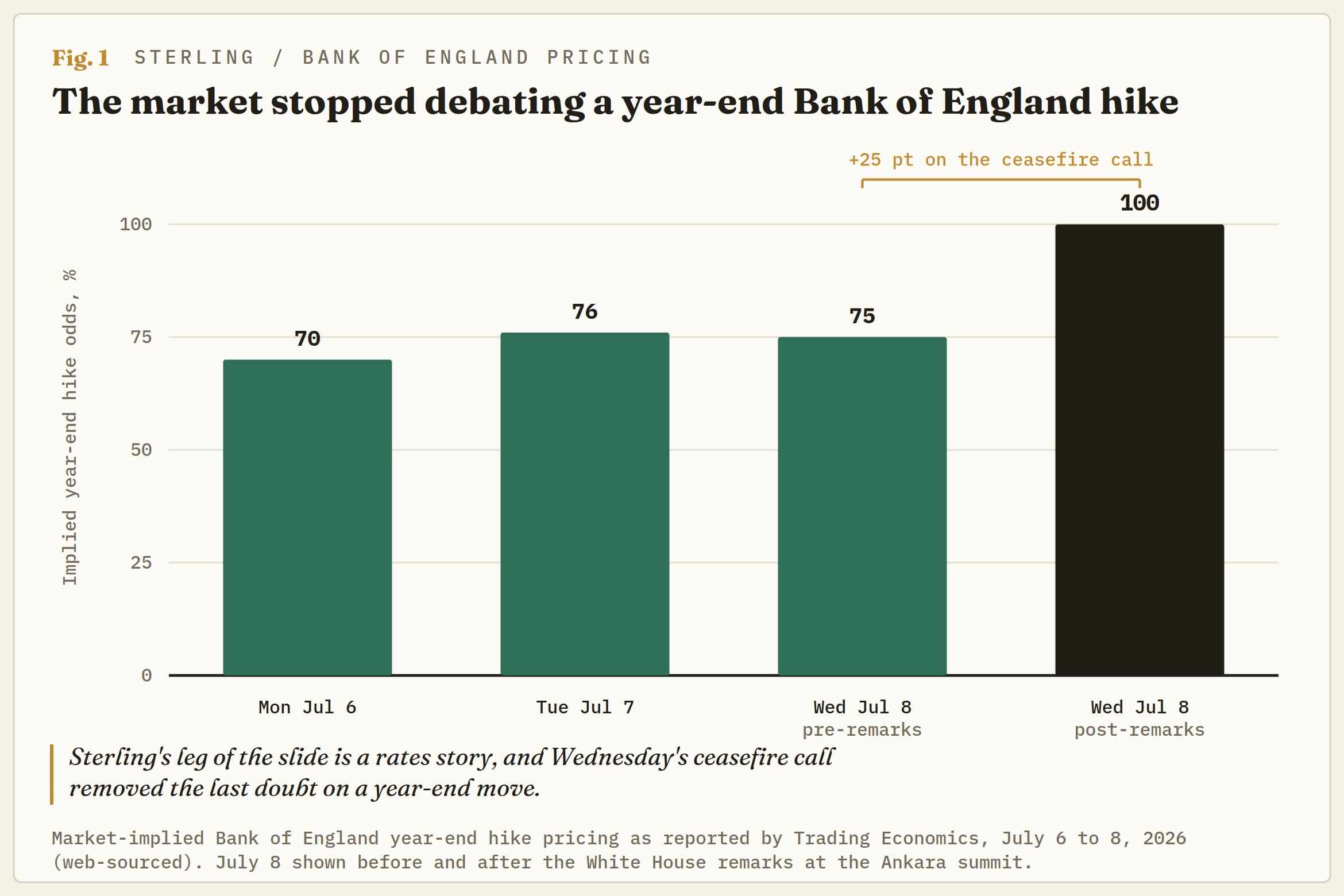

Interest rate expectations moved decisively in the Pound’s favour inside a single week. Markets priced roughly a 70% chance of a Bank of England (BoE) hike by year-end on Monday, nudged that to 76% on Tuesday, then moved to full pricing after the White House declared the ceasefire with Iran over at the North Atlantic Treaty Organization summit in Ankara. Fresh strikes sent Brent Crude Oil to a two-week high, an inflation problem a gas-heavy United Kingdom cannot wave through.

The domestic backdrop was tilting hawkish before the geopolitics intervened. June’s hold at 3.75% carried a 7-2 vote, with the chief economist and an external member preferring a move to 4.00%, one dissent more than April’s split. Services inflation is running at 3.7% against a 2.8% headline print, the Governor has ruled out near-term cuts, and the Monetary Policy Committee’s most hawkish external member booked three speaking slots inside two days this week.

A leadership vacuum would normally command a currency risk premium, yet Sterling has refused to pay one. Andy Burnham remains the frontrunner for the premiership and has yet to name a finance minister, with Ed Miliband circulating as the likely pick, while markets take reassurance from signals that the incoming leadership will keep the existing fiscal rules. Even Tuesday’s Financial Stability Report, with its warnings on equity leverage and cyber risk, left the Pound unmoved.

The European Central Bank talked hawkish all week and the market shrugged

The Euro’s side of the ledger is not dovish on paper. The European Central Bank (ECB) delivered its first hike since 2023 in June, lifting the deposit rate to 2.25% and revising its 2026 inflation projection up to 3.0% on the energy shock. This week’s speaker circuit pressed the same message, with Monday’s executive board remarks scoring well above the speaker’s own hawkish average and a Governing Council member long counted among the doves surprising hawkish on Tuesday.

Wednesday brought a third above-average hawkish reading, this time paired with a reminder that policy typically looks through one-off energy price shocks, and the Euro barely registered the remarks. June’s flash inflation estimate cooled, and the urgency went with it; pricing for a September follow-up has drifted toward a coin flip from the three additional hikes markets carried into June’s meeting. Rhetoric without a data trail behind it is being faded, and the Euro is wearing the result.

Monday’s data run handed the doves their material. Producer prices ran hot at 5.9% on the year against a 5.7% consensus, but retail sales missed on the month and Sentix investor confidence, while improving sharply, stayed negative at -3.1. An economy the ECB itself expects to grow 0.8% this year is a thin platform for a hiking cycle, however loudly the hawks audition for one.

Two meetings will now arbitrate the differential

The calendar hands the argument back to the central banks themselves. The ECB decides on July 23 and the BoE follows on July 30, with the policy gap sitting near 150 basis points in the Pound’s favour after opening the year closer to 225. Spring spent months narrowing that cushion; the last two weeks have flipped the direction of expected travel, and the cross has moved with it.

The crowding is now the trade’s main vulnerability. A hike that is fully priced is a hike that can only disappoint, and there is more room for the BoE to underdeliver on July 30 than for the ECB to out-hawk a market that has stopped listening to it. Seven declines in eight sessions have left daily momentum stretched enough that any wobble in the rate story gets amplified on the way back up.

Technical levels and bias

Resistance: Wednesday’s rejected spike at 0.8555 is the first ceiling ahead of the 0.8600 round figure, and the broader structure stays capped by the falling 50-day Exponential Moving Average (EMA) near 0.8628 with the 200-day EMA close behind at 0.8655.

Support: The fresh low at 0.8519 is all that stands before the 0.8500 handle, the last round-figure defence before the daily chart runs out of visible history.

Bias: Lower. A daily Stochastic Relative Strength Index reading near 7.55 is deeply oversold and warns of squeezes back toward 0.8550 or even 0.8600, but the trend, the rate differential, and the repricing behind both point the same way; rallies remain for selling below 0.8600 with the 0.8500 handle the next objective.

EUR/GBP daily chart

Euro FAQs

The Euro is the currency for the 20 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day.

EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy.

The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa.

The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control.

Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency.

A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall.

Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period.

If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.