The Indian Rupee has weakened sharply since the Iran-US conflict escalated, hitting a record low of 96.96 against the US dollar on May 20. On Tuesday, the rupee was trading at 95.43 against the US dollar in early trade.

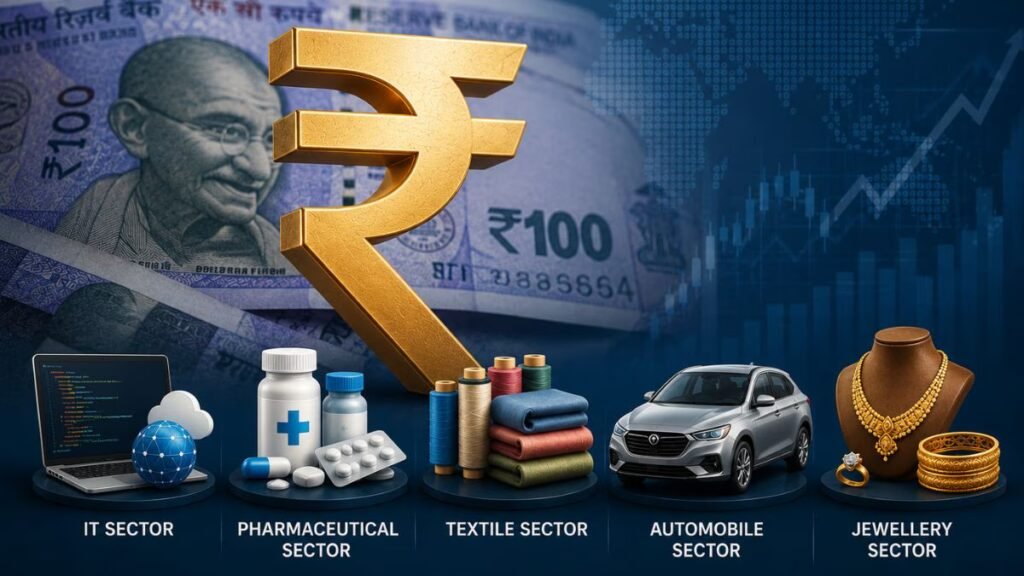

The depreciating rupee is increasing cost pressures for import-dependent sectors such as automobiles and jewellery, while export-oriented industries like IT, pharmaceuticals and textiles are expected to benefit from improved competitiveness and better dollar realisations.

Analysts said the weakening currency could support margins for exporters, but rising import costs of raw materials, electronics, precious metals and battery components may weigh on profitability across several domestic-focused sectors.

Here’s the outlook for India Inc amid the rupee depreciation.

1. IT sector: Partly offset slower revenue growth and improve margins

IT services sector could emerge as one of the key beneficiaries of rupee depreciation due to its export-oriented business model. Depreciating Rupee can improve the IT sector margins.

Sumit Pokharna, VP – Fundamental Research at Kotak Securities said, “We expect margins to remain resilient for most companies in FY27. One of the reasons is further rupee depreciation, along with tight cost control. That will partly compensate for weaker revenue growth. As a result, EPS may see upgrades in a few cases.”

However, Pokharna said that it will also depend on their exposure to different countries, because the cross currency also plays a key role. He noted that the extent of hedging by companies also matters.

Shashwat Singh, Fundamental Analyst, Bajaj Broking noted that this profits and margins windfall due to currency translation may fade over time

Singh said, “Indian software exporters are reaping an immediate revenue windfall, as a weaker rupee provides a lucrative cushion that instantly converts into expanded operating margins and short-term earnings upgrades. However, this currency party faces a clear expiration date; in the long run, macro-pressured Western clients will inevitably hit the bargaining table to aggressively renegotiate pricing and claw back these benefits.”

Sunny Agrawal, Head of Fundamental Research at SBI Securities, believes that overall impact of rupee depreciation is Neutral to Positive as, “companies may pass on some of the currency benefit to clients to sustain the deal momentum.”

2. Pharmaceutical: Sector may outperform, EBITDA tailwinds from weak rupee

Pharmaceutical exporters with strong overseas exposure are also likely to benefit from rupee weakness in the near term.

Shashwat Singh, Fundamental Analyst at Bajaj Broking said companies with global drug sales are witnessing immediate top-line gains due to better export realisations.

“However, the long-term catch, however, lies on the supply side, where prolonged currency weakness will heavily inflate the cost of imported raw Active Pharmaceutical Ingredients (APIs), squeezing margins under rigid global pricing caps,” Singh added.

Sunny Agrawal, Head of Fundamental Research at SBI Securities also noted that companies with higher exposure to US generic exposure tend to see EBITDA tailwinds. “Overall, the sector remains a defensive outperformer during INR depreciation cycles, with exporters like large-cap formulations and CRAMS players likely to outperform.”

3. Textile: Exporters see competitive advantage

The textile sector is also expected to benefit from improved export competitiveness in key markets such as the US and Europe.

According to Singh of Bajaj Broking, “Exporters are weaving immediate victories in Western markets, utilizing the depreciated rupee to capture vital market share across recovering retail landscapes in the US and Europe. Yet, these competitive volume gains face a ticking clock, as powerful global retail giants will use the currency shift as a lever to demand steep price concessions during long-term contract renewals.

Agrawal of SBI Securities said, “Export-oriented integrated players tend to benefit more than domestic-focused or fragmented players.” However, he noted that higher costs of imported synthetic materials, dyes and globally linked cotton prices may limit margin expansion.”

4. Automobile: Exporters may benefit but hurt EV makers

For the Auto sector, Rupee depreciation is going to cause a mixed impact. While export-oriented auto and auto ancillary companies benefit from better realisations and competitiveness, while import-dependent segments, especially EVs and premium vehicles, face higher input costs and margin pressure.

Neel Mehta, research associate at DRChoksey FinServ, Indian auto industry imports nearly 10–25% of its bill of materials, depending on the segment. Imported items include specialty steel, aluminium alloys, semiconductors, catalytic converter materials, lithium-ion battery cells and ADAS modules.

“A weaker rupee inflates this entire imported input basket. Costs go up, but pricing power remains limited because Indian consumers are extremely price-sensitive, particularly in the two-wheeler and entry-level car segments,” Mehta said.

He added that domestic two-wheeler makers may see only a mild impact as localisation levels remain high. However, export-oriented two-wheeler companies with significant exposure to Africa, Latin America and ASEAN markets could benefit from better competitiveness against Japanese and Chinese rivals.

Mass-market passenger vehicle makers are expected to face rising costs due to imports from Japan, Korea and China, while premium vehicle and EV manufacturers may see the sharpest impact because of heavy dependence on imported battery packs and components.

5. Jewellery: companies may turn to gold recycling amid margin stress

The jewellery sector is among the worst hit, as rupee depreciation, coupled with the recent gold import duty hike to 15% and a surging dollar, has driven domestic prices to historic highs, choking retail demand.

Shashwat Singh, Fundamental Analyst at Bajaj Broking, said, “While this combination hurts near-term sales volumes, the long-term structural reality will heavily compress retail margins, forcing organised players to aggressively pivot toward localised gold recycling schemes to stay afloat.”

Sunny Agrawal, Head of Fundamental Research at SBI Securities, also shared the same sentiment. He noted that rupee depreciation leads to higher input costs, as India imports the majority of its gold and silver requirements.

“The resulting rise in domestic jewellery prices may dampen demand in the short term, particularly in price-sensitive segments. However, companies with higher gold metal loan exposure, superior gold exchange ratios, strong brand equity that enables better price pass-through, and effective inventory hedging strategies are better positioned to navigate these cost pressures,” Agrawal noted.

Conclusion

The sharp depreciation in the rupee is helping export-oriented industries such as IT, pharmaceuticals and textiles. These sectors are to see near-term gains through better export realisations, improved competitiveness and margin support. However, analysts caution that many of these benefits could moderate over time due to pricing renegotiations, higher imported input costs and global demand pressures.

On the other hand, import-dependent sectors such as automobiles and jewellery are facing rising raw material and component costs, squeezing margins and weakening consumer demand in price-sensitive segments. Analysts believe the overall impact of rupee weakness will ultimately depend on companies’ export exposure, localisation levels, pricing power and hedging strategies.