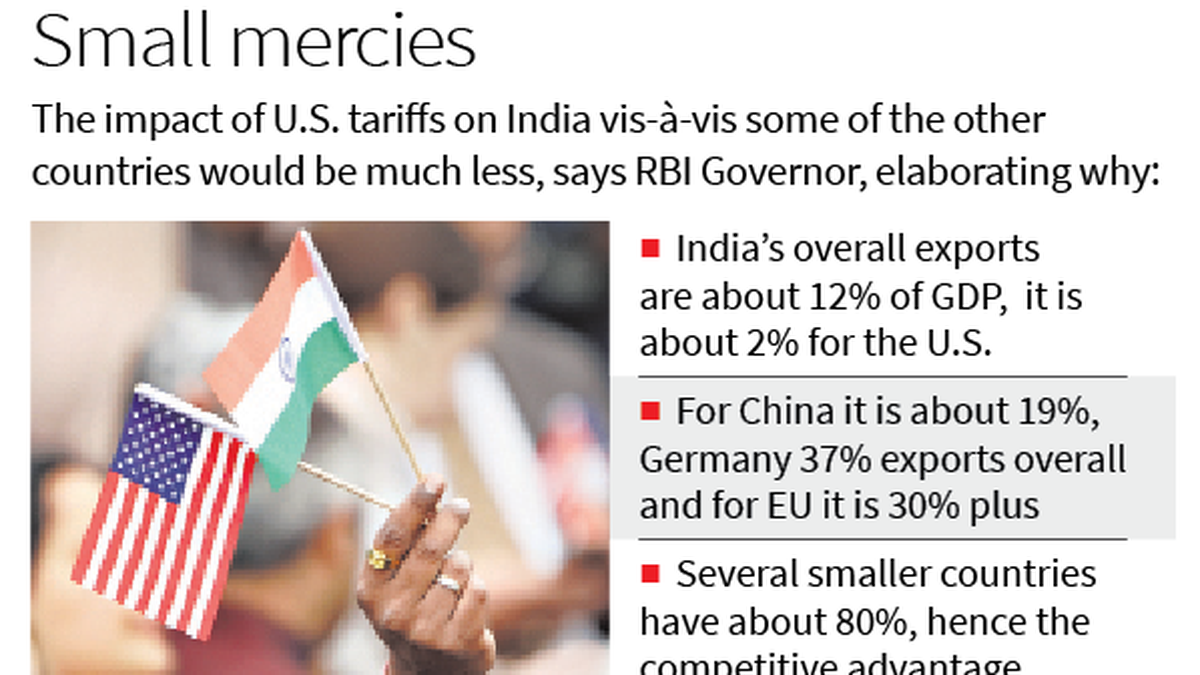

- Japanese Yen attracts some sellers during the Asian session on Wednesday, though it lacks follow-through.

- Hawkish BoJ expectations and sustained safe-haven buying help limit any meaningful downside for the JPY.

- Fed rate cut bets keep the USD bulls on the defensive and further act as a headwind for the USD/JPY pair.

The Japanese Yen (JPY) trades with a negative bias during the Asian session on Wednesday, though the lack of follow-through selling warrants some for bearish traders amid hawkish Bank of Japan (BoJ) expectations. In fact, the Summary of Opinions from the BoJ’s September meeting reaffirmed expectations that the central bank will stick to its policy normalization path. This, along with rising geopolitical tensions and concerns about the US government shutdown, acts as a tailwind for the safe-haven JPY.

Meanwhile, bets for an imminent BoJ rate hike mark a significant divergence in comparison to expectations that the US Federal Reserve (Fed) will lower borrowing costs twice this year. The latter undermines the US Dollar (USD) and the resultant narrowing of the US-Japan rate differential could benefit the lower-yielding JPY. This warrants caution before confirming that the USD/JPY pair’s corrective slide from the 150.000 psychological mark, or the highest level since August 1, touched last week, has run its course.

Japanese Yen benefits from divergent BoJ-Fed outlooks and flight to safety

- Japan’s Manufacturing PMI for September was finalized at 48.5, down from 49.7 in the previous month and marking the fastest pace of contraction in six months. That said, the Bank of Japan’s Tankan survey signaled a slight improvement in business sentiment among large Japanese manufacturers for the second consecutive quarter. In fact, the Tankan Large Manufacturers’ Index increased from 13 to 14 during the July-September period.

- This comes on top of the BoJ Summary of Opinions from the September meeting released on Tuesday, indicating increasing pressure from hawks to normalise policy, and keeps the door open for an imminent rate hike. Traders are still pricing in the possibility of a 25-basis-point rate hike by the BoJ in October, which continues to act as a tailwind for the Japanese Yen and limits the downtick witnessed during the Asian session on Wednesday.

- Meanwhile, a Republican spending bill failed to pass through the Senate on Tuesday, leading to a partial US government shutdown starting midnight. A prolonged shutdown could have an adverse effect on economic performance and set the stage for a more aggressive policy easing by the US Federal Reserve. According to the CME Group’s FedWatch Tool, traders are pricing in a greater chance of two Fed rate cuts in October and December.

- On the economic data front, the US Bureau of Labor Statistics (BLS) reported in the Job Openings and Labor Turnover Survey (JOLTS) on Tuesday that the number of job openings on the last business day of August stood at 7.22 million. The reading was slightly above the 7.2 million estimated, though it does little to impress the US Dollar bulls or assist the USD/JPY pair to build on its modest intraday move up to the 148.20-148.25 region.

- Traders now look forward to Wednesday’s US economic docket – featuring the release of the ADP report on private-sector employment and the ISM Manufacturing PMI. The US Labor Department said Monday its statistics agency would halt data releases – including Friday’s closely-watched Nonfarm Payrolls (NFP) report – if a partial government shutdown occurs, leaving the USD at the mercy of comments from influential FOMC members.

USD/JPY could accelerate decline below 147.00

From a technical perspective, the USD/JPY pair’s intraday uptick on Wednesday falters ahead of the 200-day Simple Moving Average (SMA). Some follow-through selling below the overnight swing low, around the 147.65 region, could pave the way for deeper losses and drag spot prices to the 147.20-147.15 zone. This is followed by the 147.00 mark, which, if broken decisively, might shift the near-term bias in favor of bearish traders.

On the flip side, momentum back above the 200-day SMA, currently pegged around the 148.40 area, is likely to confront resistance near the 149.00 round figure. A sustained strength beyond the latter could allow the USD/JPY pair to surpass an intermediate barrier near the 149.40-149.45 region and make a fresh attempt to conquer the 150.00 psychological mark.

Bank of Japan FAQs

The Bank of Japan (BoJ) is the Japanese central bank, which sets monetary policy in the country. Its mandate is to issue banknotes and carry out currency and monetary control to ensure price stability, which means an inflation target of around 2%.

The Bank of Japan embarked in an ultra-loose monetary policy in 2013 in order to stimulate the economy and fuel inflation amid a low-inflationary environment. The bank’s policy is based on Quantitative and Qualitative Easing (QQE), or printing notes to buy assets such as government or corporate bonds to provide liquidity. In 2016, the bank doubled down on its strategy and further loosened policy by first introducing negative interest rates and then directly controlling the yield of its 10-year government bonds. In March 2024, the BoJ lifted interest rates, effectively retreating from the ultra-loose monetary policy stance.

The Bank’s massive stimulus caused the Yen to depreciate against its main currency peers. This process exacerbated in 2022 and 2023 due to an increasing policy divergence between the Bank of Japan and other main central banks, which opted to increase interest rates sharply to fight decades-high levels of inflation. The BoJ’s policy led to a widening differential with other currencies, dragging down the value of the Yen. This trend partly reversed in 2024, when the BoJ decided to abandon its ultra-loose policy stance.

A weaker Yen and the spike in global energy prices led to an increase in Japanese inflation, which exceeded the BoJ’s 2% target. The prospect of rising salaries in the country – a key element fuelling inflation – also contributed to the move.