Financial markets are entering one of the most important weeks of the month, with Federal Reserve and Bank of England policy decisions due over the next 48 hours. While expectations are firmly centred on unchanged interest rates, investors are increasingly focused on what policymakers signal about inflation, growth and the timing of future rate cuts.

For Sterling, the backdrop remains broadly supportive. UK wage growth has remained elevated, inflation is still above target and last week’s weaker GDP data has done little to alter expectations that the Bank of England will remain cautious about easing policy too aggressively. Meanwhile, the easing of Middle East tensions and lower oil prices have helped stabilise broader market sentiment.

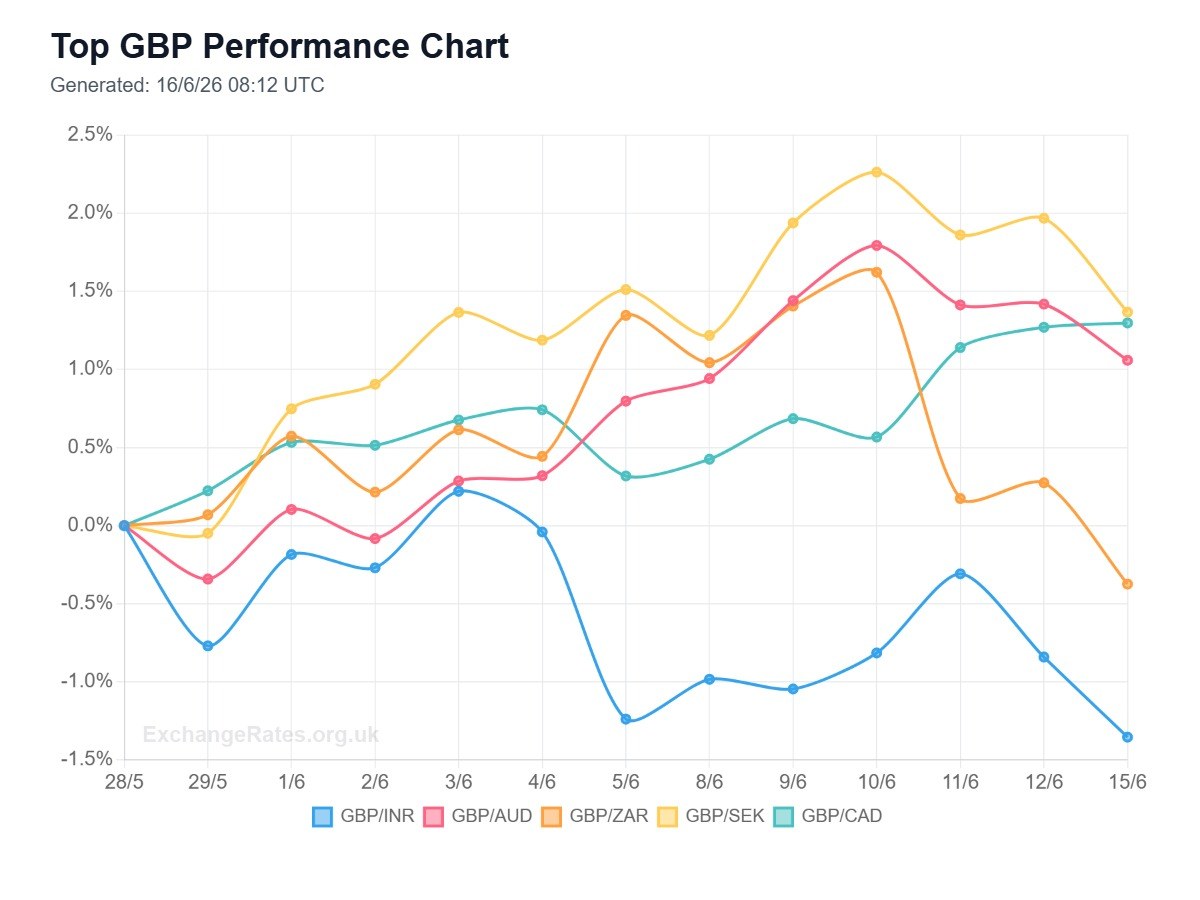

Pound Sterling‘s strongest performances this month continue to come against the Norwegian Krone, New Zealand Dollar and Australian Dollar, while the Euro and Swiss Franc have remained relatively resilient as investors balance growth concerns against expectations for central bank policy.

GBP/USD – 1.341484 (-0.00%)

The Pound to Dollar exchange rate continues to consolidate around the 1.34 level ahead of Wednesday’s Federal Reserve policy decision. The Dollar lost some safe-haven demand following reports of a preliminary US-Iran peace framework, while softer US inflation readings have reduced expectations for additional tightening. Attention now turns to whether Fed Chair Warsh signals that rate cuts remain possible later this year. GBP/USD remains comfortably above May lows, although still around 3% below January’s 2026 peak at 1.3858.

GBP/EUR – 1.156671 (-0.06%)

GBP/EUR has drifted lower since last week’s ECB meeting, with the Euro benefiting from expectations that inflation risks could remain elevated despite softer growth. Markets continue to digest the ECB’s latest guidance while also preparing for Thursday’s Bank of England announcement. Sterling remains close to the strongest levels seen this year and continues to hold above the important 1.15 support area.

GBP/JPY – 214.985920 (-0.00%)

The Pound remains close to multi-month highs against the Japanese Yen as yield differentials continue to favour Sterling. Although the easing of geopolitical tensions has reduced demand for safe-haven currencies, investors remain cautious ahead of this week’s central bank decisions. GBP/JPY remains within 1% of the 2026 high at 216.60 and continues to reflect strong carry-trade demand.

GBP/AUD – 1.900462 (+0.18%)

GBP/AUD has regained the 1.90 level after recovering strongly during June. The Australian Dollar has found support from improved risk appetite and hopes that Chinese stimulus measures will support growth. However, expectations that UK rates will remain relatively elevated continue to underpin Sterling. Traders will also be monitoring Chinese economic releases later this week given Australia’s close trade links with China.

GBP/CAD – 1.879661 (+0.13%)

The Pound to Canadian Dollar exchange rate remains close to its highest level of the year. Lower oil prices following the reported peace framework in the Middle East have reduced support for the Canadian Dollar, while Sterling has remained supported by UK interest rate expectations. GBP/CAD is now trading just below its 2026 high at 1.8813 and remains one of Sterling’s strongest-performing major crosses.

GBP/CHF – 1.066088 (+0.02%)

GBP/CHF remains broadly stable as improving market sentiment reduces demand for traditional safe havens. The Swiss Franc continues to benefit from its defensive characteristics, but Sterling’s yield advantage remains attractive. The pair has gained more than 1.3% during June and remains comfortably above levels seen earlier this spring.

GBP/NZD – 2.303925 (+0.06%)

The Pound to New Zealand Dollar exchange rate remains one of Sterling’s strongest performers this month. The New Zealand Dollar has benefited from improving global sentiment, but concerns surrounding Chinese growth and global trade continue to limit gains. GBP/NZD remains more than 2.4% higher this month and continues to trade near the strongest levels since March.

GBP/CNY – 9.067226 (-0.00%)

Sterling continues to consolidate against the Yuan as markets assess China’s growth outlook and the likelihood of additional policy support from Beijing. Investors remain cautious following a mixed run of Chinese economic data. Although GBP/CNY remains down almost 4% year-to-date, the pair has stabilised significantly after the heavy losses recorded earlier in 2026.

GBP/SEK – 12.595161 (-0.13%)

GBP/SEK has eased after reaching fresh yearly highs last week. The Swedish Krona has found support from improving European sentiment and hopes that growth conditions may stabilise across the region. Nevertheless, Sterling remains comfortably ahead on both a monthly and annual basis.

GBP/NOK – 12.796694 (+0.04%)

The Norwegian Krone remains under pressure despite recovering oil prices, allowing GBP/NOK to continue its strong June performance. The pair has risen almost 3% this month, although it remains down more than 5% year-to-date. Traders continue to weigh support from energy exports against concerns over European growth and global trade activity.

GBP/SGD – 1.719847 (-0.07%)

GBP/SGD remains trapped within a relatively narrow range as the Singapore Dollar tracks broader US Dollar movements and Asian growth expectations. Investors remain focused on Fed policy and the outlook for global trade, both of which play an important role in Singapore’s export-oriented economy.

GBP/INR – 126.753014 (-0.27%)

The Pound to Indian Rupee exchange rate has retreated as lower oil prices improve India’s economic outlook. As a major energy importer, India stands to benefit significantly if crude prices remain subdued. The Rupee has also been supported by continued capital inflows and optimism surrounding India’s medium-term growth prospects, although Sterling remains more than 4.5% higher year-to-date.

GBP/TRY – 62.110839 (+0.01%)

GBP/TRY remains close to record highs as persistent inflation and economic uncertainty continue to weigh on the Turkish Lira. Turkey’s inflation problem remains one of the highest among major economies, while investors continue to question the sustainability of the country’s economic adjustment programme. The pair remains more than 7% higher so far in 2026.

GBP/HKD – 10.507202 (-0.03%)

GBP/HKD remains broadly stable as Sterling trades sideways against the US Dollar. The pair continues to derive direction primarily from Fed expectations and broader Dollar sentiment. Sterling’s resilience above 1.34 against the Dollar is helping GBP/HKD remain comfortably above the 10.50 level.

Today’s Key Events: June 16, 2026

- UK labour market data and wage growth figures.

- Market positioning ahead of Wednesday’s Federal Reserve decision.

- Positioning ahead of Thursday’s Bank of England announcement.

- Further developments surrounding the proposed US-Iran peace framework.

- Oil price movements and inflation expectations.

- European and US bond market performance.

- Global equity market sentiment and risk appetite.