AS THE West Asia crisis continues to put pressure on the capital account, internal deliberations among policymakers in Delhi and Mumbai over the last few weeks have underlined the counter effects of “artificial stabilisation” of the rupee that preceded the slide that began in 2025.

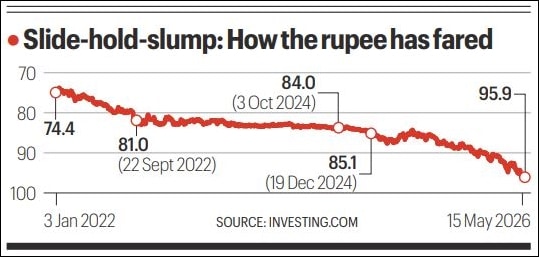

On Friday, the rupee fell past the 96-per-dollar mark, hitting a new record low. The reason why the ghosts of the past have come to haunt today is the steep slide in the exchange rate of the domestic currency. The rupee is down 5.2% against the dollar since the war began in late February and the prospects of it breaching the psychological barrier of 100 has turned real. Policymakers fear this may further hurt investor sentiment.

“It’s like past ghosts are haunting us,” a top official told The Indian Express. “If you see the levels for the years 2023 and 2024, the rupee did not depreciate much and forex was burnt to keep it stable. It was artificially held back for so long. The next psychological level is, of course, 100. And if it crosses that level, then it may slide further,” the official said.

Policymakers see the currency remaining under pressure going ahead, especially as the ability of interventions to defend any particular level are seen as limited.

According to another person aware of the discussions, the forex market is now pricing in the depreciation that may have occurred in the earlier phase of exchange rate stability, when interventions from the Reserve Bank of India (RBI) had increased significantly. This period of stability has led to the current fall in the rupee appearing steeper, the person said.

“If you see the curve of rupee’s value over the last 2-3 years, it plateaued within a narrow range. The effects of the long, artificial stabilisation then are being felt now,” he said.

After breaching the 81-per-dollar mark for the first time in September 2022, the rupee moved in a narrow range of 81-83 per dollar for the next two years or so. It broke past 84 in October 2024 and 85 in December 2024. Since the start of 2025, the rupee is down 11%.

Story continues below this ad

The RBI’s stated policy is that it does not target any specific level of the exchange rate and only steps in the market to prevent excessive volatility and ensure orderly movement in either direction: up or down.

However, people aware of the RBI’s forex market interventions in 2023 and 2024 disagree with these assertions, arguing that there was a huge Balance of Payments (BoP) surplus at the time which was exerting upward pressure on the rupee. Moreover, the rupee weakened in 2024-25 in line with the long-term trend.

The BoP is the difference between the money Indians send abroad to pay for imports and make investments and the money India receives from overseas for exports and in the form of remittances and what foreigners invest in India – be it in the stock market and bonds or direct investment in the form of factories on the ground.

As India buys more goods and services from abroad than it sells overseas, it suffers from what is called a trade deficit. However, in most years, it is more than able to make up for this trade deficit thanks to the money that flows in from abroad as investments and remittances. When these foreign fund flows are greater than the trade deficit, the BoP is in surplus, which strengthens the rupee. A negative BoP weakens the rupee.

Story continues below this ad

In 2022-23, India witnessed a deficit of $9 billion in 2022-23 and the rupee weakened by 7.6% against the US dollar, with the RBI selling then a record $213 billion as its forex reserves declined by $29 billion.

In 2023-24, the BoP moved sharply into surplus to the tune of $64 billion, forcing the RBI to not only reduce its gross dollar sales but buy $41 billion of foreign currency on a net basis, leading to the forex reserves increasing by $68 billion. The rupee, meanwhile, declined by 1.4%.

In 2024-25, the BoP moved back to a deficit of $5 billion and the rupee fell by 2.5%, largely in line with the average 3.2% depreciation witnessed in the previous 10 years. The RBI’s gross sales jumped to a record $399 billion.

According to economists, it is difficult to say if the rupee’s current travails have been exacerbated by how the exchange rate moved in previous years.

Story continues below this ad

“I think it’s hard to make that assertion with great confidence. For one, in 2023, the rupee would have appreciated and the RBI didn’t allow for that too much and built reserves instead. In 2024, it would have depreciated and instead RBI used the built-up reserves to defend the exchange rate at more stable levels,” said Lavanya Venkateswaran, Senior ASEAN Economist at Singapore-based OCBC Bank.

“I think irrespective of what happened in 2023-24, the rupee would be under pressure today. The question may be whether the levels would be this high, but it’s hard to play with a counterfactual argument,” she said.

Going by current trends, economists are increasingly of the opinion that 100-per-dollar is a “very imminent possibility, either next year or even this year”. Rajeswari Sengupta, Associate Professor of Economics at Mumbai’s Indira Gandhi Institute of Development Research (IGIDR), said attempts to stop the rupee from depreciating as per market forces “can backfire as the issues are structural – band-aids can’t heal a deeper wound”, adding that “fundamental issues” need to be addressed and structural measures are required to attract foreign capital.

At the same time, the continued depreciation is undermining measures being undertaken to stem the rot. In a report on Friday, State Bank of India Group Chief Economic Advisor Soumya Kanti Ghosh said the rupee has already approached a “critical depreciation threshold” beyond which further currency weakness could substantially erode the intended benefits of domestic fuel price hikes announced last week. “…further rupee depreciation can exhaust all these gains by increasing the $ price of crude imports. Our calculations show that, even an additional depreciation of Rs 2 in the rupee raises the effective crude oil price, pushing the landed import cost, which fully offsets the gains from the current fuel price hike,” he said.