[SINGAPORE] Investors are expected to favour major South-east Asian currencies, with economists projecting continued gains against the US dollar through the year – even as regional central banks signal further rate cuts.

These currencies remain somewhat under-appreciated amid cautious sentiment, noted Maybank analysts, but market conditions are appearing increasingly supportive.

“As more trade deals are struck, investors would get more clarity regarding the global situation and, in time, appetite towards emerging market assets, such as those in Asean, can improve,” said the Jul 28 report.

This is thanks to a softening US dollar.

Recall that the greenback remains weighed down by bearish sentiment after having notched its worst first-half slump in more than five decades of 10.7 per cent. As at Jul 31, the US dollar index has since pared a fraction of its losses but is still nursing an 8 per cent slide in the year to date.

As investors shift away from US assets, higher-yielding emerging market bonds become attractive options – and even more so when their currencies are expected to appreciate.

A NEWSLETTER FOR YOU

Friday, 8.30 am

Asean Business

Business insights centering on South-east Asia’s fast-growing economies.

“Over the years, the rupiah’s downward trend has actually eroded returns for Indonesian government bonds but, this year, the situation is looking to change,” said the Maybank analysts, adding that Malaysian government securities could see stronger inflows too.

In the Philippines’ case, US dollar softness may mean cheaper imports, which would improve the archipelago’s persistent trade deficit, reducing demand for foreign currency and in turn support the peso.

Additionally, the tariff dust is settling for some South-east Asian countries – news of Indonesia, Vietnam and the Philippines purportedly striking deals with the US played some part in offering relief to markets and lifting investor sentiment.

All things considered, the house expects the ringgit, rupiah, baht and Philippine peso all to see further gains this year.

And should investor sentiment prove less cautious and rosier than what was factored into their forecasts, the Maybank analysts see Indonesia as the biggest winner of investor flows, followed by Malaysia, Thailand and the Philippines.

Easing cycle amps up

Stabilising inflation prints, middling growth prospects and broad resilience of regional currencies against the greenback are giving central banks greater scope to trim rates.

Malaysia in July doled out its first cut in five years, calling the quarter-point reduction a “pre-emptive measure aimed at preserving Malaysia’s steady growth path amid moderate inflation prospects”.

Economists across the board agree that the dovish tone of the Jul 9 statement leaves the door open for additional policy loosening across the second half of the year to bolster growth.

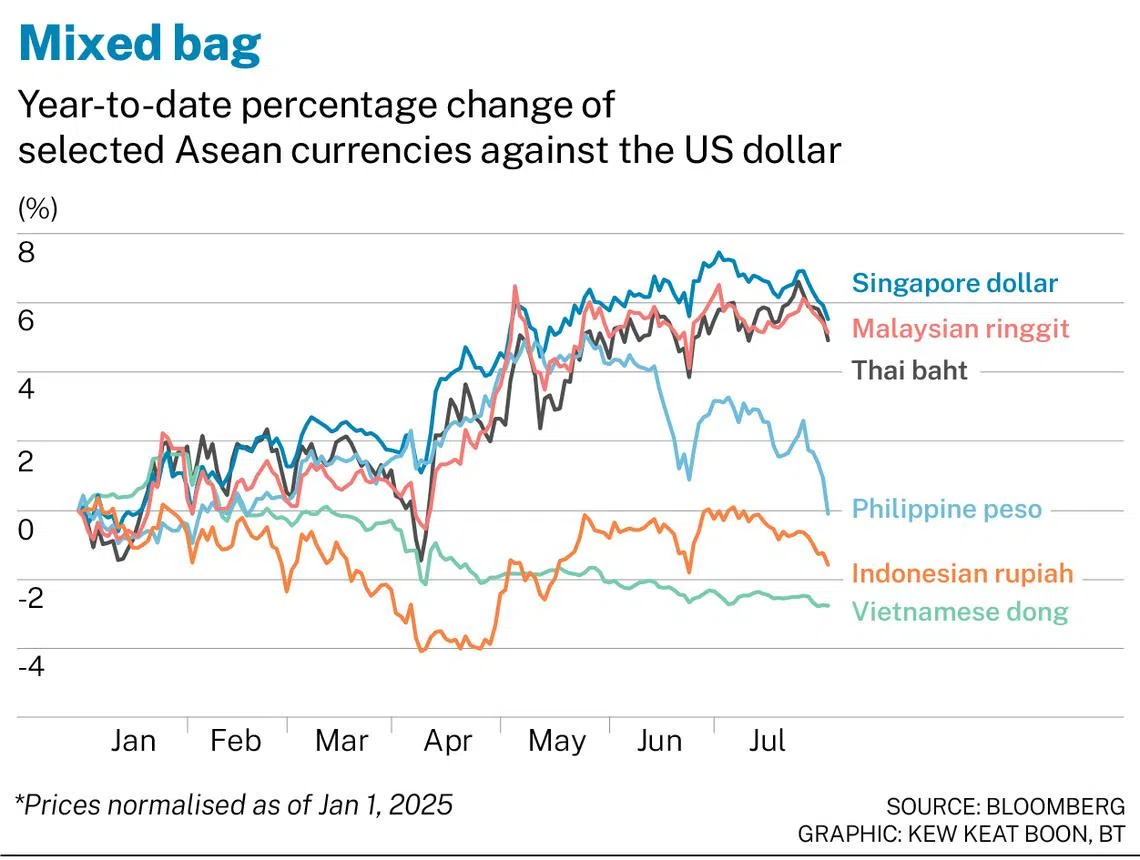

The ringgit has gained some 5 per cent against the US dollar in the year to date, and is hovering around the 4.25 level as at Jul 31.

Bank Negara Malaysia’s next monetary policy decision will be announced on Sep 4.

Indonesia the following week also dished out a quarter-point cut to its benchmark interest rate, in its third reduction of the year.

Likewise, the move was attributed to low inflation – hovering nearer the bottom of Bank Indonesia’s target range; the rupiah’s continued stability; and the need to continue stimulating economic growth.

Said DBS senior economist Radhika Rao of the cut: “Indonesian policymakers have been opportunistic this year, prudently tapping periods of market stability to lower rates, with the latest move also coming against the backdrop of the successful completion of a trade deal with the US.”

The house expects the central bank to support the rupiah through regular intervention presence, while staying bid on domestic bonds to stabilise yields, whenever necessary.

Rao added: “Baking in our baseline in-house call for the US dollar to decelerate in H2 2025, our forecast for the USDIDR is to remain stable between the 16,200 and 16,250 range.”

The rupiah is hovering around the 16,400 level as at Jul 31, having weakened some 2 per cent against the greenback in the year to date.

Economists broadly concur that more rate cuts are on the cards for Indonesia. Its next monetary policy decision will be announced on Aug 20.

As anticipated, Bangko Sentral ng Pilipinas (BSP) also cut its policy rate by 25 basis points at its latest meeting in June on a moderating inflation outlook and weaker global growth prospects. This is its second reduction of the year.

Likewise, a dovish tilt in the central bank’s statement signalled to economists the likelihood of at least one more rate cut this year.

Said MUFG senior currency analyst Michael Wan of the decision on Jun 20: “We think there’s a good chance BSP will start to intervene more aggressively if peso weakness continues unabated towards the 58 to 59 levels within a short space of time.”

The Philippine currency was hovering around the mid-57 threshold towards end-July before weakening to around 58.3 to the dollar after the US Federal Reserve left rates steady on Jul 30 (US time). It has gained some 0.5 per cent against the US dollar in the year to date.

BSP’s next monetary policy decision will be announced on Aug 28.

Thailand is among the more dovish of them all – its central bank delivered a quarter-point cut each in its first two meetings of the year, before maintaining the policy rate at 1.75 per cent in its most recent June meeting.

Its appointment of a new dovish-leaning central bank governor, delayed briefly due to incomplete paperwork, is expected to pave the way for further cuts.

Foreign exchange strategists noted in a Bank of America report that this adds another headwind to the baht in the near term as the market prices the possibility of a deeper cutting cycle.

The Thai currency’s short-term outlook is also weighed down by border clashes with neighbouring Cambodia.

But beyond the near-term volatility, the Bank of America economists believe the baht could appreciate further towards the end of the year as current account seasonality improves along with further dollar weakness. The baht has gained some 4.7 per cent against the US dollar in the year to date.

Thailand’s next monetary policy decision will be announced on Aug 13.