- The Pound Sterling corrected briefly from nearly four-year highs against the US Dollar.

- GBP/USD traders look to Fed Minutes and UK GDP data amid trade and fiscal concerns.

- Technically, GBP/USD retains upward bias so long as the daily RSI stays bullish.

The Pound Sterling (GBP) stretched its recovery mode and hit its highest since October 2021 against the US Dollar (USD) before sellers jumped in and sent the GBP/USD pair back toward the 1.3650 region.

Pound Sterling buyers faced exhaustion

After a stellar performance, spanning almost two weeks, GBP/USD buyers took a breather as exhaustion set in.

The main driver again was the dynamics of the US Dollar, but the British bond market jitters were also felt midweek, undermining the recent bullish momentum in the currency pair.

Concerns over US President Donald Trump’s ‘big, beautiful’ tax-cut and spending bill remained a major drag on the Greenback alongside uncertainty over potential US trade deals ahead of the July 9 tariff deadline.

Markets remained wary over a $3.3 trillion addition to the national debt, after the spending bill was passed by the US Senate on Tuesday and later narrowly approved by the Republican-controlled House of Representatives on Thursday,

On the trade front, the United States (US) and Vietnam reached a trade agreement on Wednesday. However, concerns about the US trade deals with Japan, South Korea, and the European Union (EU) kept the Greenback’s downside potential intact.

These worrying factors outweighed any positive impact on the buck from strong US JOLT Job Openings and ISM Manufacturing PMI data.

Further, investors pondered the timing of the next interest rate move, following Federal Reserve (Fed) Chairman Jerome Powell’s speech at the European Central Bank (ECB) Forum on central banking in Sintra on Tuesday.

Powell stuck to the bank’s ‘data-dependent’ rhetoric but said that “I wouldn’t take any meeting off the table. Can’t say if July is too soon to cut rates, will depend on data.”

The persistent downbeat mood around the Greenback drove the GBP/USD pair to nearly four-year highs of 1.3789.

However, Pound Sterling sellers quickly jumped in due to resurfacing concerns regarding the British fiscal and political situation, which sent the UK gilts in a downward spiral and GBP/USD to weekly lows of 1.3563 on Wednesday.

British Finance Minister Rachel Reeves appeared visibly upset during PMQs on Wednesday after Prime Minister Keir Starmer avoided a question if she would remain in her position until the next election.

Although Starmer’s press secretary later said that “the chancellor is going nowhere, she has the prime minister’s full backing.”

The Pound Sterling shrugged off that comment and sustained its corrective decline as the USD witnessed a relief rally on a surprisingly strong US labor market report on Thursday.

The headline Nonfarm Payrolls (NFP) rose by 147,000 in June, against expectations of a 110,000 increase and the previous revision of 144,000. The Unemployment Rate unexpectedly dropped to 4.1% last month, versus 4.3% expected and May’s 4.2%.

Solid job gains poured cold water on increased bets of US Federal Reserve (Fed) aggressive interest rate cuts this year, making the case for the Fed to hold rates steady.

The USD rebound appeared temporary on lingering concerns over deepening America’s fiscal imbalances and tariffs, keeping the downside limited for the major.

Trump said late Thursday that he “will begin sending letters on trade tariffs starting Friday.”

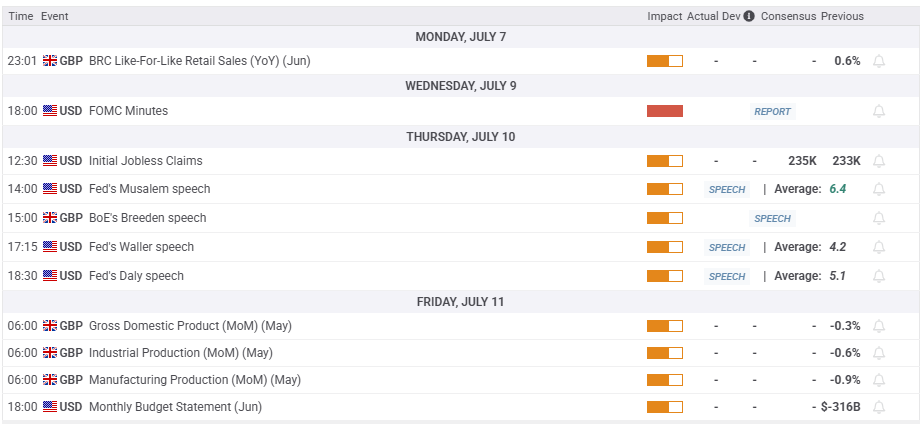

Week ahead: Fed Minutes and UK GDP on tap

Following an action-packed week, Pound Sterling traders look forward to a relatively light week in terms of top-tier economic data releases.

The early part of the week is devoid of any significant macro data and hence, the focus will remain on the potential US trade deals as the July 9 deadline approaches.

Also, of note will be the UK bond market action.

On Wednesday, the Minutes of the Fed’s June meeting will steal the spotlight, with investors still scouting for hints on the timing of the next Fed rate cut.

Thursday will feature the usual weekly Jobless Claims from the US, as well as speeches from St. Louis Fed President Alberto Musalem and BoE Deputy Governor Sarah Breeden.

The UK monthly Gross Domestic Product (GDP) report will be published on Friday alongside the Industrial and Manufacturing Production data. The US calendar that day holds only the Federal Budget Balance of relevance.

GBP/USD: Technical Outlook

GBP/USD is battling the previous resistance-turned-support of the February 2022 high at 1.3643 following a rejection above 1.3750 on several occasions.

Despite the retreat, buyers have managed to defend the 21-day Simple Moving Average (SMA) support at 1.3588 as the 14-day Relative Strength Index (RSI) continues to stay firm above the midline, currently near 57.

Therefore, sustaining above the 21-day SMA on a weekly closing basis is critical for the resumption of the GBP/USD rally.

On the upside, the immediate hurdle is seen at the 1.3750 psychological level, above which a test of the 1.3800 round level will be inevitable.

Buyers will then target the static resistance around 1.3875 on their way to the July 30 high of 1.3983.

Should the corrective downside gain traction, the 21-day SMA at 1.3588 will be the first line of defense for buyers.

Additional declines will likely attack the 1.3445 demand zone, which is the confluence of the April 28 high and the 50-day SMA.

GDP FAQs

A country’s Gross Domestic Product (GDP) measures the rate of growth of its economy over a given period of time, usually a quarter. The most reliable figures are those that compare GDP to the previous quarter e.g Q2 of 2023 vs Q1 of 2023, or to the same period in the previous year, e.g Q2 of 2023 vs Q2 of 2022.

Annualized quarterly GDP figures extrapolate the growth rate of the quarter as if it were constant for the rest of the year. These can be misleading, however, if temporary shocks impact growth in one quarter but are unlikely to last all year – such as happened in the first quarter of 2020 at the outbreak of the covid pandemic, when growth plummeted.

A higher GDP result is generally positive for a nation’s currency as it reflects a growing economy, which is more likely to produce goods and services that can be exported, as well as attracting higher foreign investment. By the same token, when GDP falls it is usually negative for the currency.

When an economy grows people tend to spend more, which leads to inflation. The country’s central bank then has to put up interest rates to combat the inflation with the side effect of attracting more capital inflows from global investors, thus helping the local currency appreciate.

When an economy grows and GDP is rising, people tend to spend more which leads to inflation. The country’s central bank then has to put up interest rates to combat the inflation. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold versus placing the money in a cash deposit account. Therefore, a higher GDP growth rate is usually a bearish factor for Gold price.