Pound Sterling climbed against the euro and US dollar, with GBP/EUR rising to 1.15001 (+0.28%) and GBP/USD advancing to 1.3462 (+0.44%), as a sharp improvement in global risk sentiment following the Iran ceasefire deal weighed on the US dollar.

Pound to Euro (GBP/EUR): 1.15001 (+0.28%)

Pound to Dollar (GBP/USD): 1.3462 (+0.44%)

Euro to Dollar (EUR/USD): 1.1706 (+0.16%)

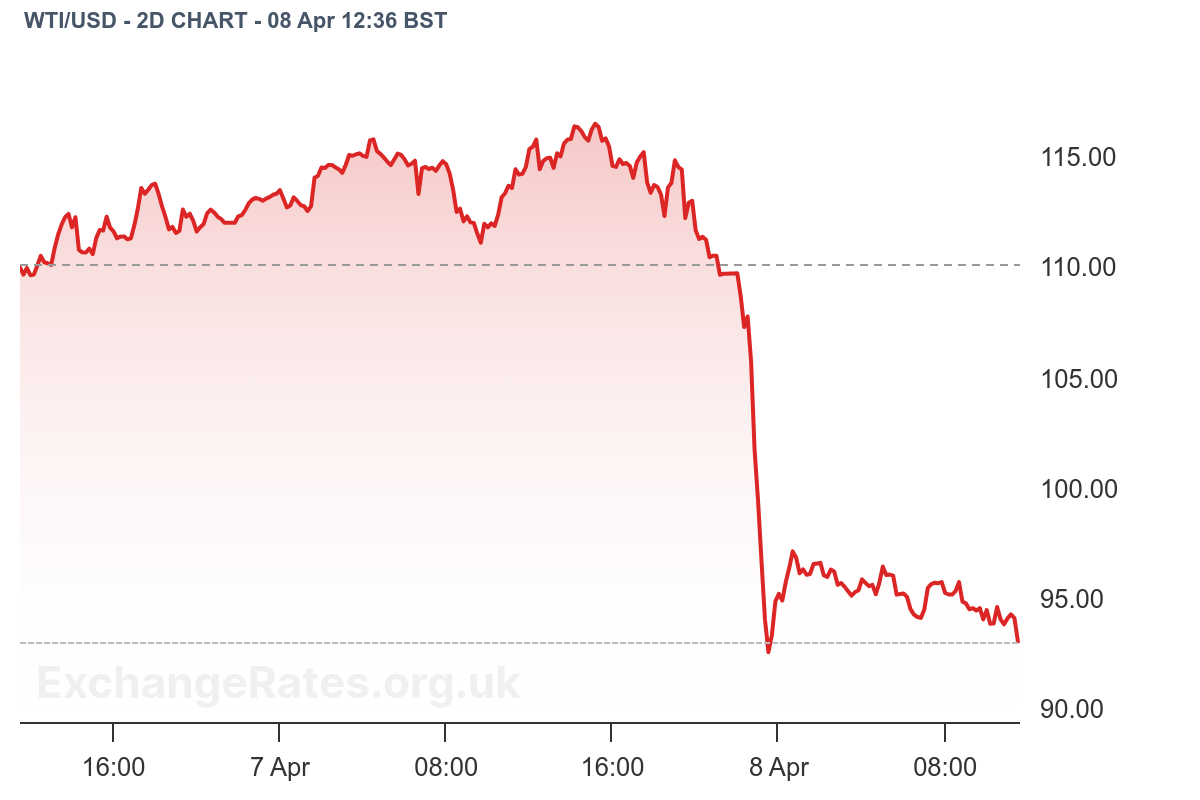

Oil prices led the move, with Brent dropping sharply from recent highs near $110 to the mid-$90s, as markets priced in a reopening of the Strait of Hormuz.

Bond yields also fell, with US Treasuries rallying as safe-haven demand unwound. Equities surged globally, signalling a decisive shift back to risk-on positioning.

SEB said the agreement marks a clear de-escalation, though its durability remains uncertain.

“The United States and Iran have agreed to a two-week ceasefire,” the bank noted, adding that markets responded immediately with lower oil prices and weaker US yields.

Crucially, Iran has agreed to allow shipping through Hormuz during the ceasefire, a development ING says is key for markets.

“The most impactful news… has been Iran’s announcement that it will allow safe passage,” ING said, adding that a recovery in shipping flows would likely “weigh further on oil prices”.

That shift has triggered a reversal of March’s dominant market theme — a stronger dollar driven by energy-led inflation fears and tightening financial conditions.

ING expects further USD downside in the near term.

“DXY… has gapped lower today, and a further sell-off to 98.50 looks possible,” it said, though cautioning that “it is premature to call for a full unwind”.

Still, the rebound comes with important caveats.

Lloyds warned that markets may be underestimating the longer-term impact of the disruption, even if the ceasefire holds.

“Even in the benign ‘ceasefire holds’ scenario… supply constraints could be an issue for some time,” the bank said.

Damage to energy infrastructure and disrupted supply chains mean inflation pressures may persist, particularly in gas markets where pricing remains elevated further along the curve.

That complicates the outlook for central banks.

Lloyds said markets had “overreacted” by pricing aggressive rate hikes during the escalation, but cautioned against swinging too far in the opposite direction.

“Assuming the disruption can be dismissed as a ‘blip’… looks overly simplistic,” it added.

SEB also highlighted political risks, noting that Iran’s demands — including control over Hormuz and sanctions relief — could derail talks.

“Iranian state media described the ceasefire… as a ‘Trump retreat’,” SEB said, underlining the fragile nature of the agreement.

For FX markets, the implication is a near-term USD correction rather than a trend reversal.

High-beta currencies and risk-sensitive assets are likely to outperform initially, but lingering geopolitical uncertainty and persistent inflation risks should keep volatility elevated.

The dollar’s safe-haven premium may have eased, but it has not disappeared.