Pound Sterling heads into the final trading day of the week close to three-month highs against the US Dollar after disappointing US jobs data triggered a broad sell-off in the greenback.

With US markets closed for Independence Day, trading conditions are expected to be quieter, although thin liquidity could amplify any unexpected moves.

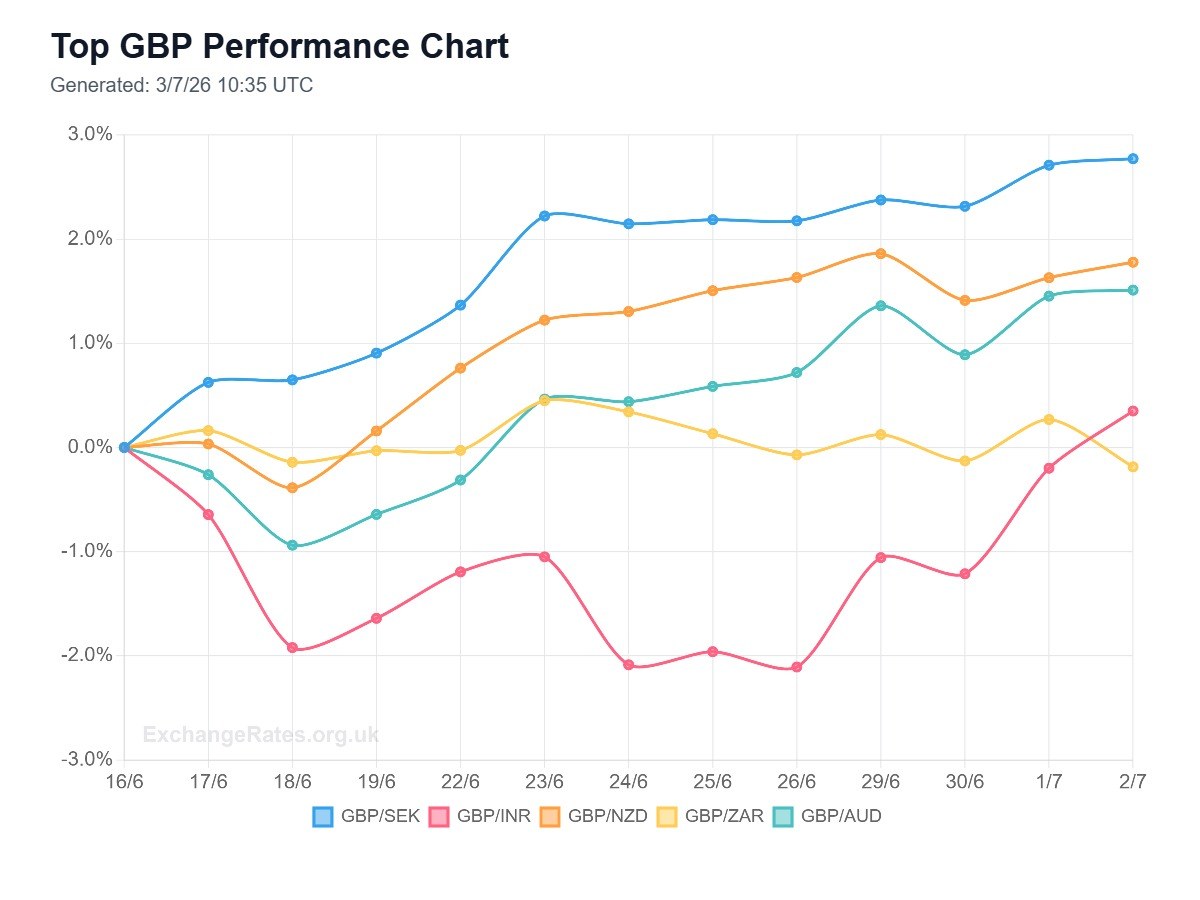

Attention is also turning back to the UK economy after political concerns eased this week, helping Sterling post its strongest weekly performance since early April.

The Pound‘s best overnight performance came against the US Dollar and Hong Kong Dollar, while the New Zealand Dollar, Swedish Krona and Australian Dollar outperformed Sterling.

GBP/USD – 1.335620 (+0.13%)

The Pound to Dollar exchange rate remains close to two-week highs after June’s US payrolls report showed the labour market cooled far more sharply than expected. Markets have responded by scaling back expectations of another near-term Federal Reserve rate hike, weighing on Treasury yields and the dollar.

Pound Sterling has also benefited from improving confidence in the UK’s fiscal outlook, leaving GBP/USD on course for its strongest weekly advance in almost three months.

The focus now shifts to Bank of England commentary and next week’s Fed minutes.

GBP/EUR – 1.166794 (-0.08%)

Pound Sterling eased modestly against the euro after a strong run higher earlier in the week.

The single currency has been supported by broad US dollar weakness, allowing EUR to recover across much of the market despite mixed Eurozone data.

With few major UK releases before next week’s GDP and labour market updates, GBP/EUR is likely to remain driven by relative interest-rate expectations.

The pair continues to trade close to its highest levels of 2026, suggesting underlying Sterling demand remains intact.

GBP/JPY – 215.184475 (-0.08%)

The Pound edged slightly lower against the Yen after Japan’s currency recovered from 40-year lows amid renewed intervention speculation.

Softer US yields have reduced pressure on the Yen, while Japanese officials have repeated that they remain ready to respond to excessive currency moves.

Even so, the wider trend still favours Sterling while UK interest rates remain well above Japanese levels.

Any renewed jump in US Treasury yields could quickly restore upward momentum in GBP/JPY.

GBP/AUD – 1.924524 (-0.22%)

GBP/AUD slipped as improving global risk sentiment supported higher-beta currencies, including the Australian Dollar. Softer US employment data has eased fears of further Fed tightening, encouraging investors back into commodity-linked currencies.

Australia’s economic outlook also received support from resilient regional activity data earlier in the week.

GBP/CAD – 1.894198 (+0.07%)

Pound Sterling continued to edge higher against the Canadian Dollar as lower oil prices limited demand for the commodity-linked currency.

Brent crude has retreated sharply from last month’s highs as concerns over Middle East supply disruption have eased, removing an important source of support for CAD.

With US markets closed, energy markets could remain the main driver into the weekend.

A sustained move above 1.8950 would leave GBP/CAD close to fresh year-to-date highs.

GBP/CHF – 1.072381 (-0.06%)

The Pound was little changed against the Swiss Franc as improving market sentiment reduced demand for traditional safe-haven assets.

Global equities have responded positively to softer US interest-rate expectations, although lingering geopolitical risks continue to underpin the Franc on dips.

Sterling retains an advantage through relatively high UK interest rates, but GBP/CHF is likely to remain rangebound unless risk appetite deteriorates or Bank of England expectations shift materially.

GBP/NZD – 2.337044 (-0.28%)

The New Zealand Dollar outperformed Sterling as investors rotated back into growth-sensitive currencies following the weaker US payrolls report.

Lower US yields and a softer dollar have improved sentiment towards the Kiwi, while markets are also beginning to look ahead to next week’s Reserve Bank of New Zealand policy decision.

Despite today’s pullback, Sterling has enjoyed a strong run against the New Zealand Dollar over recent weeks and broader technical momentum remains constructive.

GBP/CNY – 9.060979 (+0.06%)

Pound Sterling edged higher against the Chinese Yuan as the softer US Dollar continued to dominate global currency markets.

Investors remain cautiously optimistic that improving trade flows and stabilising Chinese economic data will support regional growth, although concerns over domestic demand continue to limit Yuan gains.

With US markets closed and China’s policy stance remaining accommodative, GBP/CNY is likely to take its direction from broader dollar sentiment over the coming sessions.

Today’s Key Events: July 3, 2026

- UK Final Services PMI.

- Speech by Bank of England Governor Andrew Bailey.

- Speech by ECB President Christine Lagarde.

- US markets closed for Independence Day, creating thinner trading conditions.

- Markets continue to digest Thursday’s weaker-than-expected US non-farm payrolls report and its implications for Federal Reserve policy.