Just as Mark Twain quipped that the report of his death “was an exaggeration,” it appears that reports about the demise of the U.S. dollar have also been exaggerated.

In the early days of the Donald Trump administration, many commentators speculated that this version 2.0 of Trump economics could threaten the global hegemony of the greenback — a dominance that has declined over the decades — and the huge advantages it gives the country in managing its public debt. However, amid the noise, antics, trade wars, and endless contradictions, Washington is quietly making moves to reinforce its dominance.

In short, a push to “Make the Dollar Great Again” is underway. The administration is aggressively developing the stablecoin market — a type of cryptocurrency with a stable value that serves as an alternative payment system to traditional currency — almost all of which are pegged to the U.S. dollar. This boom, which has already reached astronomical figures, represents a new form of indirect dollarization.

Meanwhile, as the Financial Times reported earlier this month, senior government officials have explored the possibility of encouraging other countries to adopt the dollar, as Ecuador and El Salvador did 25 years ago, and have held meetings to that effect with various experts, including Steve Hanke, a veteran inflation and currency specialist at Johns Hopkins, known in some circles as the “Money Doctor.”

Hanke confirmed the meeting to EL PAÍS, which took place precisely amid turbulence in Argentina, while emphasizing — as the government did when the information first emerged — that no decisions have been made yet. “While the Trump administration has a well-articulated policy on dollar-based stablecoins, it still needs to establish a more comprehensive strategy to promote the use of the dollar,” he said.

Stablecoins are virtual currencies, like all cryptocurrencies, but designed to maintain a less volatile value and are pegged to a specific asset. They are used for exchanging other cryptocurrencies, paying for goods, and sending money internationally. Today, 99% of all stablecoins in circulation worldwide — which total $225 billion, according to JPMorgan — are denominated in dollars. It is a kind of digital dollar, but issued by the private sector, unlike the initiatives in the Eurozone or Beijing.

By 2028, some reports suggest that this market could reach $3 trillion. Washington has been very explicit about its expectations for the new currency. Last July, the Genius Act — the U.S. law regulating digital assets and their growth — was passed decisively. At the time, Treasury Secretary Scott Bessent stated that this type of technology “will buttress the dollar’s status as the global reserve currency, expand access to the dollar economy for billions across the globe, and lead to a surge in demand for U.S. Treasuries, which back stablecoins.” He added that it “could also spur millions of new users across the globe to the dollar-based digital asset economy.”

When the financial world talks about the “exorbitant privilege” of the dollar, it largely refers to the demand for U.S. public debt that Bessent mentioned. This refers to the lower cost at which the United States can finance its massive debt, which exceeds 120% of its gross domestic product (GDP). The country already pays more in debt interest than it does on Defense. And stablecoins are backed by Treasury bonds.

How strong is the dollar’s dominance today? Today, the dollar represents 58% of total foreign currency reserves worldwide (the euro, in second place, barely reaches 20%). That nearly 60% is indeed a notable dominance, but it pales in comparison to the 1970s, when it exceeded 80%, and it also represents the lowest level in the past two decades. Its preeminence has eroded, and while Trump has played with fire on trade, this does not mean that any currency could realistically dethrone the dollar in the foreseeable future.

As Joseph Gagnon, a finance expert at the Peterson Institute for International Economics in Washington, explains: “Currently there are only two possible competitors: the euro and the yuan. People are afraid to trust their money to the Chinese, whose authorities maintain strict controls on moving capital in and out of the country. Europe is too fragmented to challenge the dollar; it needs more unified banking, financial, and tax systems, with a large central budget and a single Treasury, like in the United States […] When this happens, the dollar will face real competition.”

Cryptocurrencies, of course, do not appear to be the path for the euro to surpass the dollar. Santiago Carbó, professor of Economics at the University of Valencia in Spain, warns of the danger that Europe could “miss the train” with digital currencies. “Visa and Mastercard are already American. If you also don’t get on the stablecoin wave, you’re going to be left far behind in the global payments system market.”

Beyond virtual currencies, there are other ways to promote the use of dollars, explains Steve Hanke. One is what is known as a “currency board,” in which the national currency is issued and exchanged at a fixed rate with the dollar and fully backed by it. Another is direct dollarization, which involves replacing the original currency with the U.S. dollar. Drawing on his experience with projects such as the dollarization programs in Montenegro (1999) and Ecuador (2000), among others, Hanke advocates for a policy that addresses all three possibilities. In his view, this would not only provide an advantage for the United States, but also for the countries that adopt it.

It is a widely debated issue. For Gagnon, dollarization represents “an act of desperation” by some economies, one that is “difficult to reverse,” and he doubts that any country will pursue it. In some countries, it has served as a form of discipline and helped control inflation, but it also means adopting the Federal Reserve’s monetary policy and restricts countries’ ability to handle crises. At the same time, the flood of stablecoins complicates capital controls and the possibility of currency depreciation.

The president of the European Central Bank (ECB), Christine Lagarde, has warned against the rise of these cryptocurrencies, which are particularly attractive for enabling faster and cheaper international transactions. “These assets are not always able to maintain their fixed value,” she said last June in a hearing before the European Parliament. She also cautioned that a potential shift from banks to stablecoins in deposits used for savings and payments “could adversely affect the transmission of monetary policy through banks,” meaning that central bank measures could have a diminished effect on the real economy. For this reason, she called for strong regulation.

At the same time, the euro’s global role has grown in importance in Frankfurt. “The changing landscape [referring to Trump’s protectionist turn] could open the door for the euro to play a greater international role,” she said just a month earlier in Berlin. The digital euro has also become a priority on the European Union’s financial agenda.

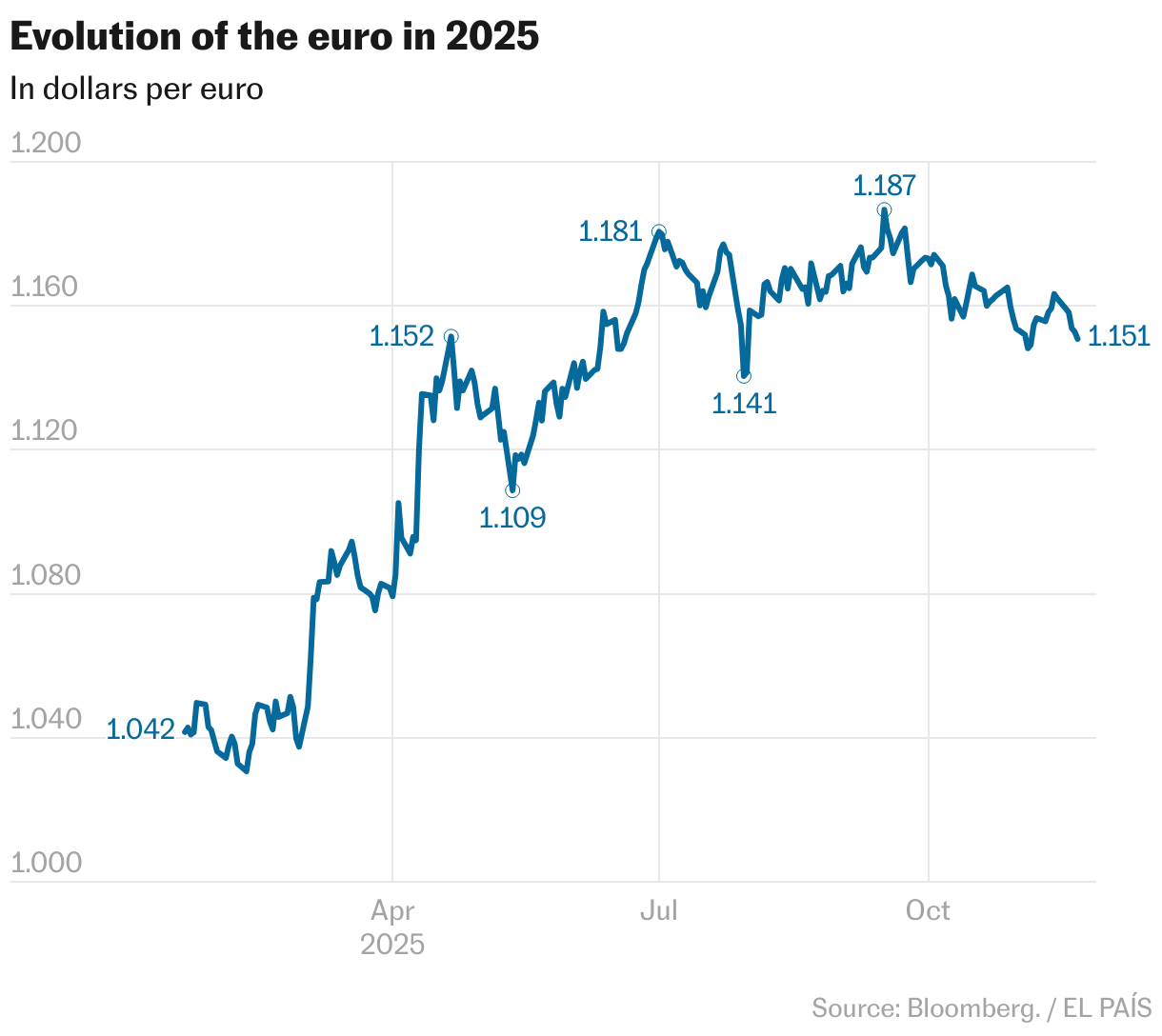

Indeed, as with so many things in the Trump universe, the strategy to boost the dollar’s hegemony contradicts other policies of his administration. Its value fell by around 10% against other major currencies in the first half of the year and, specifically against the euro, has not recovered to the level prior to the announcement of the major tariff wave on April 2 of this year, the so-called “Liberation Day” (see chart).

A cheaper dollar would help reduce the trade deficit that so frustrates Trump, but it clashes with the desire to preserve the “exorbitant privilege.” So what is the priority? While tariff policies and the push for dollar-backed stablecoins may seem inconsistent with each other, they serve a common purpose: both help finance the fiscal deficit. Moreover, crypto could make the Trump family, which has heavily invested in it, immensely wealthy.

Sign up for our weekly newsletter to get more English-language news coverage from EL PAÍS USA Edition